How to Calculate HRA: A Complete, Practical, and Policy-Aware Guide

House Rent Allowance (HRA) is one of the most important components of an employee’s salary structure and a vital element in personal tax planning. Understanding how to calculate HRA accurately helps salaried individuals claim the right exemption, optimize their tax liability, and align housing costs with broader financial goals. This long-form article explains how to calculate HRA step-by-step, traces the history and policy framework around HRA, examines state-wise and regional impacts, discusses successes and challenges, compares HRA with other housing benefits and social welfare initiatives, and lays out future prospects. Read on for a comprehensive, authoritative resource that shows precisely how to calculate HRA and why it matters.

Introduction: Why HRA Matters and what this guide covers

House Rent Allowance is provided by many employers to compensate employees for rental accommodation costs. Beyond compensation, HRA has a tax-exempt portion under income tax laws in several jurisdictions, which means knowing how to calculate HRA can reduce taxable income significantly. This article covers not only the arithmetic of how to calculate HRA but its legal basis, policy objectives, regional variations, and intersections with initiatives like rural development and women empowerment schemes that influence housing choices and affordability.

Throughout, we use clear examples and plain language so that whether you are a finance professional, HR practitioner, or an employee planning your budget, you will understand how to calculate HRA, how the exemptions work, and how HRA interacts with broader policy frameworks and state-wise benefits.

A brief history and objectives of HRA

HRA has roots in the evolution of modern salaried employment. As urbanization increased and employers sought standardized salary structures, employers began providing allowances for rent. Over time, tax systems recognized HRA as a necessary part of living costs, and tax exemptions or deductions for HRA were introduced to ease housing burdens on salaried workers.

The main objectives behind HRA and related policy choices include:

- Providing cost-of-living support for employees, especially in urban areas.

- Encouraging formal rental arrangements and improving housing market functioning.

- Aligning employer compensation with social policy, such as state-level housing allowances and social welfare initiatives.

- Reducing tax burdens on middle-income earners through targeted exemptions.

Understanding these objectives clarifies why governments regulate HRA exemptions and why knowing how to calculate HRA is important for both compliance and planning.

The policy framework and statutory context

HRA’s treatment in tax law is typically set by national tax statutes and influenced by administrative rules. While specifics vary by country, common elements include:

- Definition of taxable salary and exempt allowance.

- Conditions for claiming HRA (for example, proof of rent paid, whether the employee lives in rented accommodation).

- Caps on exemption amounts based on salary, rent paid, city classification, or a percentage of basic salary.

Within this policy framework, how to calculate HRA becomes a technical exercise governed by statutory formulas and documentation requirements. The interlinkage with state welfare schemes, urban housing policies, and measures to boost affordable rental housing means that interpretations of HRA can vary regionally. Therefore, professionals should view how to calculate HRA not only as arithmetic but as an application of the relevant policy framework.

Core concept: What components affect HRA calculation

Before diving into detailed formulas, it’s essential to know the variables that affect how to calculate HRA:

- Basic salary (or basic salary plus dearness allowance, depending on local rules).

- Actual HRA paid by the employer.

- Actual rent paid by the employee.

- Location or city category (metro/non-metro) because some laws offer higher exemptions for higher-cost cities.

- Any statutory caps or percentage limits.

Armed with these variables, you can follow the standard approach to determine the exempt portion and the taxable portion of HRA.

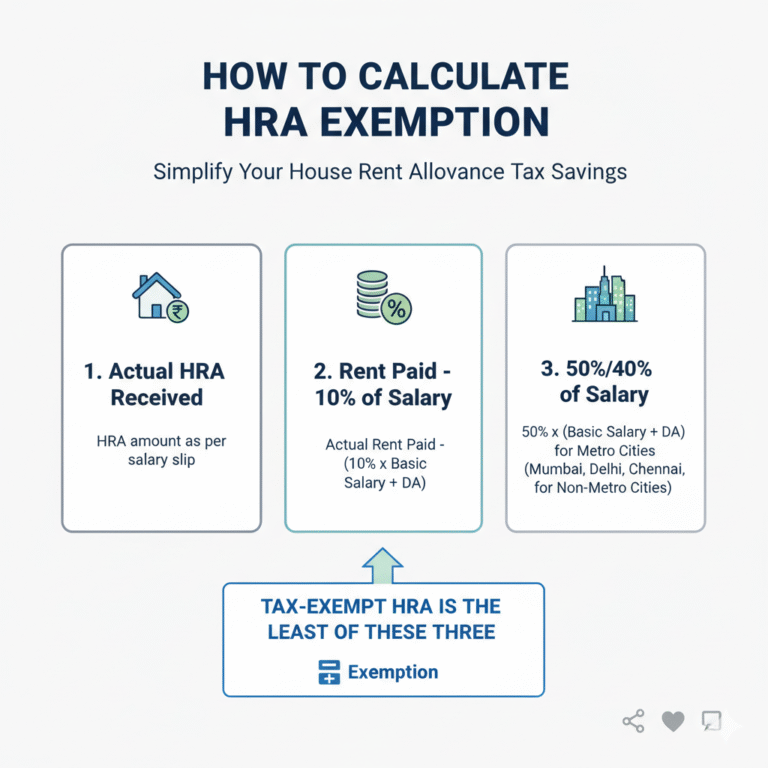

How to calculate HRA: Standard formula and step-by-step method

The calculation method described here reflects the most common statutory approach where the exempt portion of HRA is the minimum of three values. This method is widely used in jurisdictions where HRA exemption is provided as the least of (a) actual HRA received, (b) actual rent paid minus 10% of salary, and (c) a percentage of salary (commonly 50% for specified metro cities and 40% for non-metro cities). Below is the step-by-step process explaining how to calculate HRA.

- Identify your annual basic salary (or basic plus dearness allowance if statute includes DA).

- Identify the total HRA paid by your employer in the fiscal year.

- Sum up the total rent paid by you for the fiscal year.

- Determine your city type (metro or non-metro) as defined by the local tax rules.

- Compute three amounts:

- Amount A = Actual HRA received from employer (annualized).

- Amount B = Rent paid (annualized) minus 10% of salary (annualized).

- Amount C = Percentage of salary (50% if metro, 40% if non-metro, unless statute says otherwise).

- The exempt HRA is the minimum of A, B, and C. The remainder of the HRA received is taxable.

This step-by-step description is the practical prescription on how to calculate HRA. Below, we illustrate with worked examples and then discuss documentation and real-world issues.

Practical examples: Worked calculations to show how to calculate HRA

Example 1: Metro city, basic salary ₹600,000 annually, HRA paid ₹180,000 annually, rent ₹240,000 annually.

- Amount A = Actual HRA = ₹180,000.

- Amount B = Rent paid − 10% of salary = ₹240,000 − (10% of ₹600,000 = ₹60,000) = ₹180,000.

- Amount C = 50% of salary = 50% of ₹600,000 = ₹300,000.

- Minimum of A, B, C = min(₹180,000, ₹180,000, ₹300,000) = ₹180,000.

- Exempt HRA = ₹180,000. Taxable HRA = Actual HRA − Exempt HRA = ₹0.

This example demonstrates simply how to calculate HRA when rent and HRA align.

Example 2: Non-metro city, basic salary ₹720,000 annually, HRA paid ₹150,000, rent ₹120,000.

- Amount A = ₹150,000.

- Amount B = ₹120,000 − (10% of ₹720,000 = ₹72,000) = ₹48,000.

- Amount C = 40% of salary = 40% of ₹720,000 = ₹288,000.

- Minimum = min(₹150,000, ₹48,000, ₹288,000) = ₹48,000.

- Exempt HRA = ₹48,000. Taxable HRA = ₹150,000 − ₹48,000 = ₹102,000.

These examples show concretely how to calculate HRA using the statutory minima approach. Note that minor jurisdictional differences (such as inclusion of DA in salary) will affect computation.

Documentation and compliance for HRA claims

Correctly documenting your rent and ensuring compliance is as important as knowing how to calculate HRA. Typical documentation includes:

- Rent receipts showing landlord name, PAN (where required), and period of tenancy.

- Rental agreement or lease deed.

- Employer declaration (in some cases).

- Bank statements or transactional proofs of rent payment.

Authorities may require PAN of the landlord if rent paid exceeds statutory thresholds. Knowing how to calculate HRA must go hand-in-hand with maintaining appropriate proof to substantiate exemptions.

State-wise and regional impact of HRA policies

HRA does not operate in a vacuum; regional housing markets and state-level policies influence both the need for HRA and its effective benefit:

- In high-rent metropolitan areas, higher HRA exemptions are often allowed (for example a higher percentage of basic salary) reflecting higher living costs.

- State-level housing schemes, rent-control regulations, and targeted subsidies interact with HRA. For instance, regions with active state housing programs or women empowerment schemes that include housing benefits can reduce reliance on HRA or alter rental market dynamics.

- Rural development and urban migration trends change demand for rental housing. As rural development programs improve rural infrastructure and employment, pressure on urban rental markets may moderate, indirectly influencing HRA relevance.

When considering how to calculate HRA, also consider how regional cost-of-living and state benefits modify the lived reality for employees.

HRA and social welfare initiatives: intersections and synergies

HRA often intersects with social welfare initiatives and broader housing strategies:

- Governments may run affordable housing, slum rehabilitation, or women empowerment housing schemes that offer subsidized rents or ownership options, which shift the emphasis away from HRA reliance.

- Policy frameworks that encourage rental housing supply (for example, incentives to build rental apartments) can stabilize rents and change the optimal personal tax planning for HRA.

- HRA is sometimes used in coordination with allowances for government employees or special packages for employees in backward regions to incentivize mobility and service delivery.

Understanding how to calculate HRA in isolation is useful, but understanding how it operates alongside social policies provides a fuller picture of housing outcomes and income security.

Success stories and illustrative case studies

Across different regions, organizations and governments have leveraged allowances and policy design to improve housing affordability and service delivery:

Case study: Corporate relocation packages in a major metro city combined market-based HRA with temporary relocation allowances and housing search assistance. Employees who received clear guidance on how to calculate HRA and on claim documentation were better able to secure exemptions and reduce tax costs while the company achieved smoother talent mobility.

Case study: A state-level program that matched rental subsidies with employment placements in semi-urban centers reduced pressure on metros. Employees were educated on how to calculate HRA to align reimbursement and personal budgeting, yielding better housing affordability outcomes.

These examples underline that knowing how to calculate HRA empowers individuals to make better housing and tax decisions while complementing larger social objectives.

Challenges and common pitfalls when calculating HRA

While the formula is straightforward, several practical challenges complicate how to calculate HRA:

- Incorrect salary base: Not all users know whether dearness allowance (DA) is to be included with basic salary for the calculation.

- Missing documentation: Inadequate rent receipts or informal arrangements make it hard to substantiate claims.

- Non-standard employment arrangements: Contractors or gig workers may not receive HRA or may face ambiguity in claiming exemptions.

- State or city classification confusion: Misclassification of the city type (metro vs non-metro) can lead to miscalculations.

- Landlord PAN and compliance: Where statutes require landlord PAN for claiming deductions beyond certain thresholds, absence of PAN creates compliance issues.

Avoiding these pitfalls requires both procedural clarity and good record-keeping, the practical complements to knowing how to calculate HRA.

Comparing HRA with other housing benefits and schemes

HRA is only one piece of the housing benefits landscape. Comparing HRA with other options helps in planning:

Employer-provided housing or subsidized housing: Some employers provide accommodation or housing loans. Employer-provided housing usually has different tax implications, and knowing how to calculate HRA remains necessary to compare the tax value.

House Rent Deduction versus Home Loan Interest: Deductions for home loan interest and principal repayment encourage home ownership and have different tax mechanics. When choosing between renting and buying, employees should compute both the HRA advantage (using the method to determine how to calculate HRA) and the benefits from mortgage-related deductions.

State rental subsidies and welfare programs: These programs may provide direct subsidies. In contexts where state benefits reduce effective rent, the formula used in how to calculate HRA should factor in the net rent paid after subsidies.

This comparative perspective ensures that how to calculate HRA is used as part of a broader housing and tax optimization strategy.

Future prospects: How HRA might evolve

Housing markets and policy priorities evolve; so might the treatment of HRA:

- Greater emphasis on affordable rental housing could alter exemption formulas or documentation requirements to better target benefits.

- Digitalization of rental agreements and payments may simplify proving rent paid, making the administration of HRA claims smoother.

- Integration with state-level housing and welfare initiatives could harmonize HRA calculations with broader housing subsidies and social security nets.

- New approaches to rent indexing or cost-of-living adjustments might lead to dynamic HRA percentages by city or by inflation index.

Staying current on these trends helps employees and HR professionals understand not only how to calculate HRA today but how to adapt to future changes.

Practical tips for employees and HR teams

Employees and HR teams should follow these practical steps to ensure correct HRA treatment:

- Maintain organized rent receipts and a signed rental agreement.

- Confirm with payroll whether DA is included in the salary base for HRA computation.

- Verify your city classification under the tax rules to determine the correct percentage to use when you calculate how to calculate HRA.

- If landlord PAN is required, request it in advance and document payment proofs.

- For relocation or temporary assignments, coordinate with HR to understand whether HRA or other allowances apply.

These operational tips help transform the theory of how to calculate HRA into effective day-to-day practice.

Advanced calculation scenarios and clarifications

Several nuanced scenarios come up in real-world HRA calculations:

- Shared accommodation: If two or more employees share rental payments, exemptions may be apportioned. Knowing how to calculate HRA here involves documenting each person’s share and payments.

- Part-year residence: If an employee lives in rented accommodation for part of the fiscal year, prorate the amounts accordingly when you calculate how to calculate HRA.

- Rent paid to close relatives: Some jurisdictions limit exemptions if rent is paid to relatives, or require landlord PAN. Understand local rules before you compute how to calculate HRA in such cases.

- Employer provides accommodation: When accommodation is partially provided, the valuation of perquisites may interact with HRA rules.

In every case, the foundational skill is knowing precisely how to calculate HRA with the correct salary base, rent figures, and location percentage.

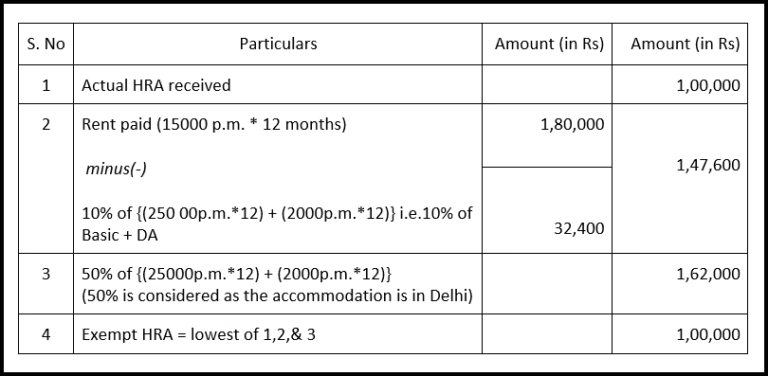

Example: A full, annotated calculation walkthrough

Consider a salaried employee in a metro city with the following annual details:

- Basic salary = ₹840,000

- Dearness Allowance = ₹60,000 (not considered for this jurisdiction’s salary base)

- HRA paid = ₹240,000

- Rent paid = ₹300,000

Step 1: Salary base = Basic salary = ₹840,000.

Step 2: Amount A = Actual HRA = ₹240,000.

Step 3: Amount B = Rent paid − 10% of salary = ₹300,000 − ₹84,000 = ₹216,000.

Step 4: Amount C = 50% of salary (metro) = ₹420,000.

Minimum of A, B, C = min(₹240,000, ₹216,000, ₹420,000) = ₹216,000.

Exempt HRA = ₹216,000. Taxable HRA = ₹240,000 − ₹216,000 = ₹24,000.

This annotated example transparently shows how to calculate HRA and how each variable affects exemption.

Practical budgeting: Using HRA calculations to plan housing choices

Understanding how to calculate HRA helps in making housing decisions:

- Rent-to-income ratio: Knowing exempt HRA helps you estimate after-tax cost of rent, making it easier to compare renting versus buying.

- Negotiating rent: If rent exceeds thresholds that give higher exemption, negotiating or sharing accommodation may increase tax efficiency.

- Relocation decisions: When offered higher HRA for relocation, calculate practical net benefits after taxation to decide whether to accept.

These budgeting strategies show the real value of mastering how to calculate HRA beyond tax returns.

FAQs — Common questions about HRA and exact answers

Conclusion: Make HRA work for you

Mastering how to calculate HRA is a practical skill with real financial impact. It reduces taxable income legitimately, improves budgeting for housing costs, and helps employees make informed choices about renting, relocating, or buying. While the arithmetic—finding the minimum of three values—is straightforward, effective application of how to calculate HRA requires good documentation, awareness of regional policy differences, and attention to special cases like shared rentals or payments to relatives.

To apply this guide, gather your salary figures, HRA receipts, and rent documentation, confirm your city classification, and follow the step-by-step formula. Use the worked examples here as templates, adapt them to local rules (inclusion/exclusion of dearness allowance or different percentages), and consult tax advisers for complex or ambiguous cases. With clear records and this practical knowledge on how to calculate HRA, you can confidently claim the exemptions you are entitled to and optimize your housing-related finances.