How to Calculate HRA Rebate: The Complete Guide for Salaried Individuals

House Rent Allowance (HRA) is one of the most commonly used salary components for tax planning among salaried taxpayers. If you’re searching for how to calculate HRA rebate, this comprehensive guide explains the rules, the step-by-step formula, documentation requirements, exceptions, comparisons with other rent-related deductions, state-level impacts, success stories, challenges, and future prospects. The aim is to give you practical clarity on how to calculate HRA rebate so you can maximize legal tax savings while meeting compliance obligations.

Understanding HRA: Purpose and policy framework

House Rent Allowance is paid by employers to employees who live in rented accommodation. The allowance is partly or wholly exempt from tax under the old tax regime subject to conditions laid out under the Income Tax Act (section 10(13A) and related rules). To answer the basic question of how to calculate HRA rebate, the law requires a comparison of three amounts and the exemption is the least of them. This mechanism makes HRA an important allowance for employees in rented homes, particularly in metro cities where rent burdens are higher. Income Tax India+1

HRA is designed as part of a broader policy framework that recognizes housing costs as a genuine expense for people who do not own residential property at their workplace or place of posting. The allowance therefore intersects with wider social welfare initiatives and labour compensation policies by supporting mobility, female workforce participation, and urban-rural economic dynamics—all of which shape how different states implement complementary measures such as affordable housing schemes and rental housing policies.

Basic eligibility: who can claim HRA exemption?

Before discussing how to calculate HRA rebate, check eligibility:

- HRA exemption applies only to salaried individuals who receive HRA as part of their salary. If you do not receive HRA (i.e., it is not part of your CTC), you cannot claim HRA; you may instead consider Section 80GG deduction if eligible.

- You must actually be paying rent for residential accommodation.

- You cannot claim HRA exemption for the period you occupy your self-owned accommodation at the same locality.

- HRA exemption is normally available under the old tax regime; the new tax regime (introduced in recent years and optionally selected by taxpayers) typically does not permit HRA exemption. Check the regime you’ve chosen, because how to calculate HRA rebate depends on the regime.

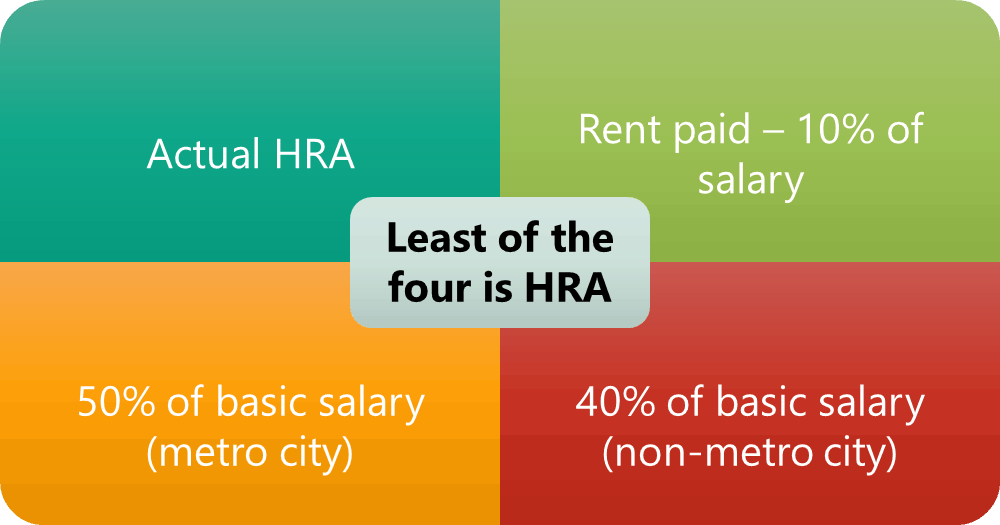

The formula — a step-by-step on how to calculate HRA rebate

When you’re ready to calculate the exemption, the law requires computing three figures and taking the minimum. This is the clearest answer to how to calculate HRA rebate in practice.

- Actual HRA received from the employer (annual).

- 50% of (basic salary + dearness allowance (if applicable)) for those living in metro cities; 40% for those living in non-metro cities.

- Actual rent paid in excess of 10% of (basic salary + dearness allowance).

The exempt amount = the least of (1), (2), and (3).

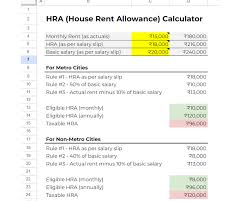

An example shows how to calculate HRA rebate step by step: suppose annual basic salary + DA is ₹300,000, actual HRA received is ₹120,000, and annual rent paid is ₹180,000. If the taxpayer lives in a non-metro city:

- (1) Actual HRA = ₹120,000

- (2) 40% of basic + DA = 40% × ₹300,000 = ₹120,000

- (3) Rent paid − 10% of basic + DA = ₹180,000 − 10% × ₹300,000 = ₹180,000 − ₹30,000 = ₹150,000

Least of (120,000; 120,000; 150,000) = ₹120,000. So the exempt portion (the HRA rebate) is ₹120,000 and any HRA beyond that is taxable. This practical scenario clarifies how to calculate HRA rebate for many salaried taxpayers.

Metro vs Non-Metro: a key distinction

The difference between 50% and 40% (metro vs non-metro) is central to how to calculate HRA rebate. Metro cities are those designated as metros by tax rules—generally the large urban centers where rents are higher. For calculation purposes, if you are posted in a metro, the allowable percentage is 50%; otherwise, it is 40%. This regional adjustment has a material effect on regional impact and equity—employees in metros get a higher notional allowance for exemption to reflect higher rental costs.

Documentation you must retain when claiming HRA

To prove your HRA entitlement (which is central to correctly understanding how to calculate HRA rebate), maintain the following documents:

- Rent receipts or bank challans showing regular rent payments (many employers and the tax authority require evidence for audit).

- A rental agreement or lease deed where applicable.

- PAN of the landlord if annual rent exceeds a statutory threshold (currently a specified amount, check the latest ITR guidance).

- Form 16 provided by your employer and a declaration to employer about rent paid (if required).

Recent practice in ITR filing requires more detailed rent and landlord disclosures so maintaining accurate records is more important than ever. Failure to maintain authentic documentation can lead to scrutiny of your HRA claims.

When HRA is fully taxable

If you live in your own house or have not paid rent to anyone, HRA received is generally taxable; the exemption is available only when you actually pay rent. Additionally, under the new tax regime, many taxpayers who opt for lower rates lose exemptions like HRA. Therefore understanding how to calculate HRA rebate requires first confirming that you’re eligible under your chosen tax regime.

Section 80GG—alternate route for those without HRA in salary

If your salary does not include HRA, you may be able to claim a deduction under Section 80GG for rent paid, subject to conditions (e.g., you or your family do not own a house in the location where you reside). Section 80GG’s rules and arithmetic are different from HRA’s, and knowing how to calculate HRA rebate must be complemented by understanding Section 80GG so you pick the option that yields the higher benefit. Section 80GG is a separate deduction and could be more beneficial for those not receiving HRA as part of salary.

Practical worked examples

Example 1 — Metro resident with HRA:

Basic salary + DA: ₹500,000 per year

HRA received: ₹200,000 per year

Rent paid: ₹240,000 per year

- (1) Actual HRA = ₹200,000

- (2) 50% × (basic + DA) = 50% × 500,000 = ₹250,000

- (3) Rent paid − 10% × basic + DA = 240,000 − 50,000 = ₹190,000

Least = ₹190,000. So how to calculate HRA rebate results in ₹190,000 exempt; taxable HRA = ₹200,000 − ₹190,000 = ₹10,000.

Example 2 — Non-metro resident: basic + DA ₹360,000; HRA ₹120,000; rent paid ₹150,000

- (1) 120,000

- (2) 40% × 360,000 = 144,000

- (3) 150,000 − 36,000 = 114,000

Least = ₹114,000 → exempt HRA ₹114,000. These hands-on computations answer how to calculate HRA rebate in practical cases.

How employers compute HRA in payroll: practicalities

Employers follow the same legal formula when computing HRA exemption for payroll and to generate Form 16 or income statements. Usually, payroll software calculates the exempt portion monthly based on year-to-date figures or projected annual figures, so the monthly HRA exemption declared in payroll may differ from the final exemption computed at the year end. If you change jobs midyear, or change rented accommodation, adjustments may affect how to calculate HRA rebate across months, so carefully reconcile Form 16 and your own calculations at the time of filing returns. Employer compliance practices and IT portal changes have also made disclosure stricter during ITR filing.

Common pitfalls and audit triggers

Knowing how to calculate HRA rebate is not only about math; it’s about compliance risk. Common mistakes include:

- Claiming HRA without supporting rent receipts or inconsistent rent proof.

- Paying rent to close relatives without documentary proof of actual payment (banks trails, cheques, or online bank transfers are needed).

- Not accounting for periods when you lived in owned accommodation or employerprovided lodging.

- Claiming HRA under the new tax regime where it’s disallowed.

Tax authorities have been more active in validating HRA claims, especially where inconsistencies appear between Form 16, ITR entries, and reported landlord income. Authenticity and consistent record keeping reduce the risk of rejection.

Integrating HRA with broader financial planning

Calculating how to calculate HRA rebate should be part of broader household budgeting and financial planning. For instance:

- Compare the tax benefit of continuing to rent (and claim HRA) versus buying a property (and claiming home loan benefits).

- Consider the impact on cash flows—rent payments are outflow with HRA partial relief; EMIs create longterm financial commitment but offer principal and interest benefits under other sections.

- Factor in state-level housing policies, subsidized housing, or rent subsidy schemes that can affect your net housing cost and thereby the practical value of HRA. LSI keywords like “state-wise benefits”, “regional impact”, and “housing policy framework” matter when making these choices.

State-wise impact and regional considerations

Regional differences—variation in rental markets, urbanization pace, and state housing policies—shape the real-world value of HRA. A ₹200,000 HRA exemption yields a different standard of living in a Tier-1 city than in a smaller town. Consequently, how to calculate HRA rebate has different practical outcomes across jurisdictions, and state governments often complement central tax policies with rental housing schemes, affordable housing projects, and incentives for women’s housing cooperatives and rural development programs that indirectly change rental patterns. For example, urban infrastructure and job hubs concentrate higher rentals in certain states, increasing the practical importance of HRA there. These contextual elements are critical for a holistic answer to how to calculate HRA rebate.

HRA and gender—women empowerment angle

HRA calculations intersect with women empowerment where women relocate for employment or education. Accessible rental accommodation and the ability to claim HRA improve mobility and lower barriers to female labour force participation. When you explore how to calculate HRA rebate, also consider supportive policies like women-only housing projects, state welfare schemes that reduce rents, and employer policies providing accommodation or HRA support to women returning to work or joining the workforce.

Comparisons with other schemes and deductions

To fully answer how to calculate HRA rebate, compare HRA with similar provisions:

- Section 80GG deduction (for those not receiving HRA in salary): the least of three different calculations (rent − 10% of total income, ₹5,000 per month, or 25% of total income). Choosing between HRA and 80GG depends on which yields a larger reduction in taxable income. TaxBuddy.com+1

- Home loan tax benefits (Section 24 and Section 80C): these benefit homeowners and are a different class of relief, so understanding how to calculate HRA rebate helps weigh renting vs owning financially.

- Standard deduction and other allowances: under the new tax regime, many allowances are removed—understanding the regime choice is crucial to decide how to optimize benefits.

Implementation challenges: what makes HRA calculation and claims difficult?

Even though the formula for how to calculate HRA rebate is straightforward, implementation and compliance can be tricky due to:

- Documentation mismatches (digital receipts vs cash payments).

- Disputes with landlords on declared rent vs actual payments.

- Changes in employer payroll handling and the difference between projected exemption and final actual exemption.

- Multiple residences during the year (e.g., relocation for work), which requires prorating exemptions correctly.

Resolving these practical issues involves careful record keeping, timely communication with employers, and in some cases, seeking the advice of a tax professional. The Economic Times

Success stories: real outcomes of correct HRA use

Across India many salaried taxpayers have improved household savings by correctly applying the HRA exemption. Common positive outcomes include:

- Young professionals in metro cities claiming HRA support during early career years, freeing savings for retirement and home down payments.

- Dual-income households where one spouse’s HRA combined with tax saving strategies reduced overall tax and enabled faster asset building.

- Workers relocating across states who used HRA calculations and careful documentation to avoid tax notices and optimize cash flows.

These success stories emphasize that knowing how to calculate HRA rebate and complying with documentation rules produce measurable financial benefits.

Technology and online calculators

Several banks and tax portals provide HRA calculators that implement the exact formula, letting you input salary, HRA, rent and city type to get a quick answer. These calculators are helpful tools when learning how to calculate HRA rebate and reconciling payroll numbers with your own records. Authoritative calculators include those from the Income Tax Department and leading financial services websites which follow statutory formulas. However, always reconcile online tool outputs with actual Form 16 and employer records before filing. Income Tax India+1

The role of payroll and Form 16—what employers report

When employers process payroll, they compute taxable HRA and report exempt HRA in Form 16. The final responsibility for accuracy rests with the taxpayer at the time of filing ITR. Understanding how to calculate HRA rebate helps you verify Form 16, ask for corrections where the exempt amount is not correctly reflected, and ensure proper disclosure on ITR schedules. With increasing disclosure requirements, mismatches are easier for tax authorities to detect, reinforcing the need for accurate calculations and record keeping. The Times of India

Litigation and disputes: what to watch for

There have been disputes when tax authorities scrutinize HRA when a landlord’s income does not reflect reported rent, or where rent receipts are deemed insufficient. While the law’s formula for how to calculate HRA rebate is clear, the evidentiary burden is often where disputes arise. Transparent, bank-traceable rent payments and valid rental agreements mitigate risk.

Future prospects: how might HRA rules evolve?

The tax environment evolves with policy goals. Potential future changes could include:

- More detailed disclosures and digital verification for HRA claims to reduce fraud.

- Adjustments to metro/non-metro classifications or percentages to reflect changing urban rental patterns.

- Greater linkage between rental subsidy policies and taxable benefits for targeted groups (e.g., women returning to work or low-income urban workers).

By staying updated with official releases and financial press, taxpayers can ensure they understand how to calculate HRA rebate under current rules and anticipate reforms.

Practical checklist: steps to correctly calculate and claim HRA

To apply the knowledge of how to calculate HRA rebate, follow this checklist:

- Confirm whether you receive HRA and whether you are under the old tax regime.

- Gather basic salary, DA, actual HRA received, and total rent paid for the year.

- Determine your city status (metro/non-metro).

- Apply the three-figure formula to find the exempt amount.

- Maintain rent receipts, lease agreements, and bank statements showing rent payments.

- Reconcile your calculation with your employer’s Form 16 and finalize ITR entries.

FAQs — Practical answers to common questions

Final thoughts: mastering the calculation and compliance

Understanding how to calculate HRA rebate empowers salaried taxpayers to legitimately reduce tax liability while ensuring compliance. The formula is straightforward, but correct application requires attention to documentation, city classification, the chosen tax regime, and state-level housing contexts. By combining accurate calculation, record keeping, and awareness of state and employer practices, you can optimize housing-related tax benefits safely and effectively.

For one-line takeaway: calculate the three figures carefully—(actual HRA received), (50%/40% of basic+DA), and (actual rent paid − 10% of basic+DA)—choose the least and keep clear evidence of rent payments. When you understand how to calculate HRA rebate, the benefit is reliable, measurable, and legally robust.