How to Calculate HRA Exemption: A Complete Guide for Salaried Individuals

House Rent Allowance (HRA) is one of the most commonly used tax exemptions for salaried taxpayers in India. Knowing how to calculate HRA exemption correctly can save you substantial tax and help you plan salary structure and housing decisions more intelligently. This comprehensive guide explains the legal basis, the exact formula, practical examples, document requirements, state-wise and regional impact, implementation challenges, success stories, and comparisons with other housing-related tax benefits. It also answers the most frequently asked questions so you can confidently claim HRA relief while staying compliant.

What is HRA and why it matters

House Rent Allowance is an allowance paid by employers to employees to help meet the cost of renting a house. Part of this allowance can be exempt from income tax under the Income Tax Act, subject to conditions. Understanding how to calculate HRA exemption matters for two reasons: first, it directly affects your taxable salary and therefore your tax liability; second, it influences financial planning — whether to rent or buy, how to split salary components, and how to document rent payments.

The rules for exemption are codified under the Income Tax Act and supporting rules; the government also provides an HRA calculator on the official income tax website to help taxpayers estimate the exempt portion. Income Tax India+1

Legal basis and brief history

The tax treatment of allowances, including HRA, has evolved over decades as India’s labour market and housing landscape changed. HRA as a specific exemption is provided under Section 10(13A) of the Income Tax Act and is operationalized through the rules in the Income Tax Rules (for example, Rule 2A and related guidance). Over time, the exemption has been refined to balance relief to taxpayers against revenue safeguards and to reduce fraudulent claims. The government also periodically tightens reporting requirements and employer verification norms to ensure authenticity. Bajaj Housing Finance+1

Core objective of HRA exemption

The principal objective of the HRA exemption is to provide tax relief to salaried employees who pay rent for accommodation. The policy aims to reduce the tax burden on employees who otherwise incur significant living costs in rented housing, especially in urban and metro areas where rents can be high. HRA also indirectly supports labour mobility — people can relocate for jobs without a disproportionate tax penalty on their housing costs. Over time, HRA has become part of salary structuring strategies used by HR and payroll teams.

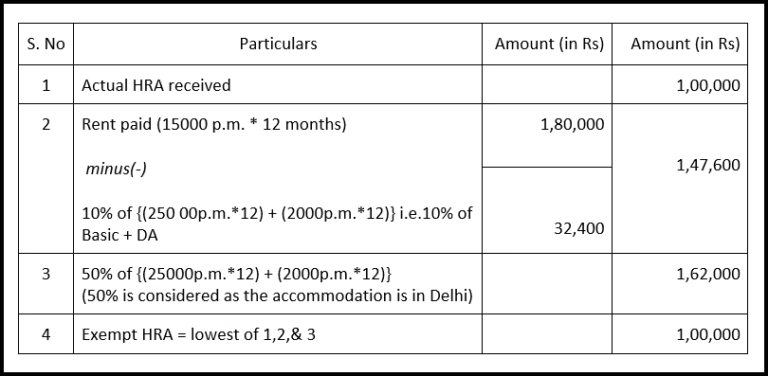

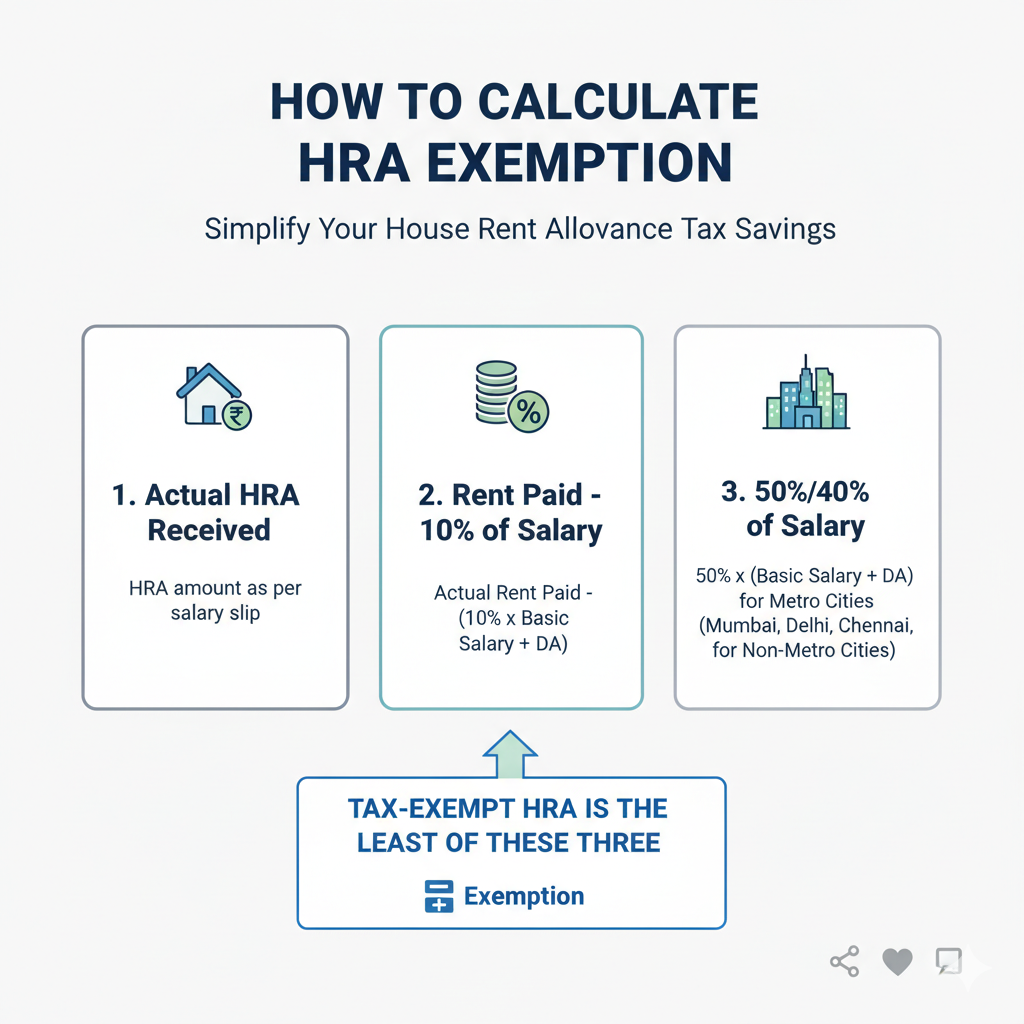

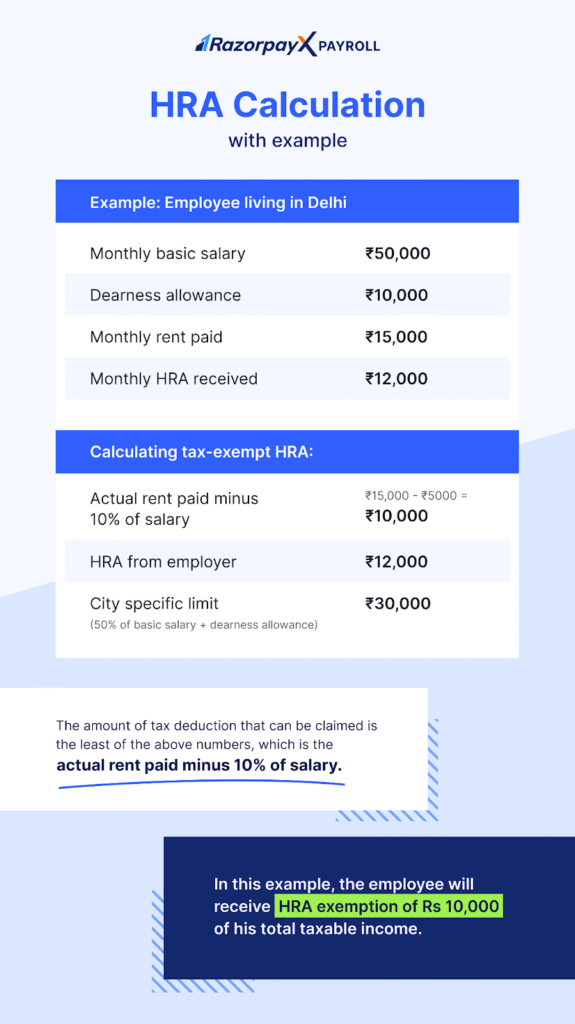

The exact formula: how to calculate HRA exemption (step-by-step)

If you want to know how to calculate HRA exemption, here’s the step-by-step method used across India. The exempt amount is the least of the following three values:

- Actual HRA received from the employer.

- Rent paid in excess of 10% of salary — i.e., (Actual annual rent paid) − (10% of annual salary).

- 50% of salary (for employees living in designated metro cities) or 40% of salary (for those living in non-metro cities).

Here, “salary” for the purposes of HRA calculation typically includes basic salary plus dearness allowance (DA) where DA forms part of retirement benefits and is fully taxable as salary for that purpose; other allowances are generally excluded unless specified. In practice most payrolls treat “salary” for HRA as Basic + DA (if applicable). The official Income Tax Department provides a calculator and guidance on this method. ClearTax+2ICICI Prudential Life Insurance+2

Worked example to illustrate how to calculate HRA exemption

Suppose:

- Basic salary + DA = ₹50,000 per month (₹6,00,000 annually)

- HRA received = ₹20,000 per month (₹2,40,000 annually)

- Rent paid = ₹15,000 per month (₹1,80,000 annually)

- City = metro (so 50% rule applies)

Compute the three figures:

- Actual HRA received = ₹2,40,000

- Rent paid − 10% of salary = ₹1,80,000 − 10% of ₹6,00,000 = ₹1,80,000 − ₹60,000 = ₹1,20,000

- 50% of salary = 50% of ₹6,00,000 = ₹3,00,000

Least of (₹2,40,000; ₹1,20,000; ₹3,00,000) = ₹1,20,000 — this is the HRA exempt amount. The remainder of HRA (₹2,40,000 − ₹1,20,000 = ₹1,20,000) is taxable as part of salary. This stepwise method is what payroll teams and tax calculators use when showing you “exempt HRA” and “taxable HRA.” ClearTax

Key definitions and clarifications for accurate calculation

When you are learning how to calculate HRA exemption, it’s essential to be clear about the definitions used in the formula:

- Salary: For HRA, salary normally refers to Basic Salary plus Dearness Allowance (if DA is part of retirement benefits). Other allowances such as conveyance, medical, or performance bonuses are typically excluded from this “salary” computation for HRA purposes. If in doubt, check your employer’s payroll definition or official guidance. ICICI Prudential Life Insurance

- Actual rent paid: The rent you actually pay to a landlord, net of any subsidies or reimbursements. If you live with family and pay nominal rent or no rent, claims can be scrutinized; legitimate evidence and bank trail are important. News reports and case law show that tax authorities sometimes challenge unsubstantiated HRA claims. The Economic Times

- Metro vs Non-metro: The 50% vs 40% rule is a standard split. Metro cities are typically defined (for HRA purposes) as major urban centers such as Mumbai, Delhi, Kolkata, and Chennai — but you should confirm current lists if you live in a city on the borderline. Different portals and institutions list the applicable metros for HRA. Housing

- Actual HRA received: This is the HRA component appearing on your salary slip for the financial year.

Practical payroll issues and examples

Payroll teams, HR professionals, and employees commonly face implementation questions when calculating HRA. For example:

- When you get HRA monthly but move mid-year from rent to owner-occupied home: you can calculate exemption on a monthly basis or annual aggregate; the employer’s computation can prorate HRA for months you paid rent. The tax department allows proportional calculations; however, documentation proving month-by-month rent payment may be requested by the employer or during an assessment.

- When you receive partial rent reimbursement in cash: only the actual documented rent payments backed by bank transfers, rent receipts, or rent agreements should be counted for HRA exemption. Employers often require rent receipts and, if requested, landlord PAN when annual rent exceeds stipulated thresholds.

- Multiple employers during the year: if you changed jobs and both employers paid HRA in the same year, you must compute the exempt portion across the full financial year using the combined HRA received and overall salary figures.

These operational points matter when you learn how to calculate HRA exemption for real-world situations — both for compliance and to maximize legitimate tax savings. Income Tax India

Documentation: what you need to claim HRA

Knowing how to calculate HRA exemption is only half the job; the other half is documentary proof. Employers typically ask for the following as proof before allowing HRA exemption through payroll or Form 12BB:

- Rent receipts for the year (monthly or annual), bearing landlord name and address, and tenant’s name.

- Rent agreement (lease deed) especially if it’s a long-term lease.

- Bank statements, NEFT/RTGS/cheque images showing rent payments — a clear audit trail reduces the chance of future disallowance.

- Landlord PAN (mandatory if annual rent paid to a single landlord exceeds a specified government threshold) — this has been enforced periodically to curb tax evasion.

- Form 12BB (for employees to submit proof of claims) as required by the employer.

Recent reporting indicates that the new ITR utility and employer scrutiny require more detailed disclosures and can subject HRA claims to verification — so robust documentation is essential. The Times of India+1

State-level and regional impact: why location matters

When you explore how to calculate HRA exemption, the concept of metro vs non-metro immediately highlights the role of geography. HRA is deliberately more generous (50% of salary) for metros because of higher rentals in large urban centers. Beyond the basic metro/non-metro split, state-level housing markets, inter-state migration patterns, and state policies affect how HRA functions:

- High-rent states and metros: Cities such as Mumbai and Delhi create stronger demand for HRA relief because housing costs form a larger portion of household budgets. Here HRA exemption plays a meaningful role in disposable income.

- Smaller cities and tier-2 towns: With lower rents, the 40% non-metro rule usually suffices; however, employees who move from metros to smaller towns for work may see different HRA benefits.

- State housing policies: State-led schemes, affordable housing initiatives, and rent-control measures can indirectly influence HRA claims by changing rent levels in a region. In states investing in affordable housing, the need for HRA relief may evolve as rents stabilize.

- Rural-urban migration and labour mobility: HRA supports workforce mobility by lowering the tax penalty of relocating for employment; this has consequences for state economies that benefit or lose skilled labour depending on HRA-driven net flows.

Layering these regional dynamics into a personal HRA computation helps answer the practical question of how to calculate HRA exemption in a way that reflects local realities. Housing

HRA, social policy and indirect linkages (regional impact, rural development)

Although HRA is a tax provision for salaried people, it ties into broader social and economic policy themes:

- Regional impact: HRA can influence where professionals choose to live, affecting urban density, public transport use, and local real estate markets.

- Rural development: While HRA targets urban renters, labour mobility enabled by tax-neutral movement of workers can indirectly help rural households via remittances.

- Women empowerment schemes & social welfare initiatives: While HRA is not a targeted social welfare measure, enabling women to work in cities and access safe housing through HRA-inclusive salaries supports financial independence. Some organizations consider HRA in designing movement and relocation allowances for women employees.

- Policy framework: HRA sits within a framework of tax policy and housing-related regulations. When governments adjust housing subsidies, rent control, or affordable housing programs, the context in which HRA operates changes. Understanding how to calculate HRA exemption therefore benefits from awareness of these larger policy currents.

These linkages show that HRA, while technical, is not isolated — it interacts with social and economic realities beyond payroll numbers.

Comparisons with other housing-related tax benefits

When considering how to calculate HRA exemption, you should also compare it with other housing tax benefits to choose the optimal financial approach:

- Principal and interest deduction on home loans (Sections 80C & 24(b)): If you buy a house with a home loan, you can claim deductions on principal repayment under Section 80C and on interest under Section 24(b). The tax impact may sometimes outweigh HRA benefits, especially for owner-occupied houses. When you switch from renting (and claiming HRA) to owning a home (and claiming loan deductions), compute total tax and cash flow implications.

- Standard deduction vs HRA: HRA is specific for rent; employees under the new tax regime may prefer standard deductions and lower slab rates. Choosing between old and new regimes requires calculating net benefits of HRA versus standard allowances.

- Conveyance and other allowances: These allowances are separate and seldom substitute for HRA. However, salary structuring with varied allowances can shift taxable income and HRA calculation; understanding how these pieces interact is vital.

Comparative analysis helps you decide whether to rent and claim HRA or buy a home and use loan-related deductions — a calculation that depends on personal goals, cash flows, and long-term planning.

Success stories: employers and employees getting HRA right

There are many practical success stories illustrating how proper attention to how to calculate HRA exemption yields benefits:

- Salary restructuring for young professionals: Employers who structure pay with a higher HRA component helped employees reduce taxable income while maintaining take-home pay. Transparent documentation and counselling reduced errors during ITR filing.

- Corporate relocation packages: Companies that combined HRA, rent reimbursement with proof, and a brief period of rent subsidy for new hires saw higher acceptance rates and faster onboarding.

- Women employees relocating for work: In several organizations, HRA combined with safe housing stipends helped women accept roles in cities, enhancing career progression.

These successes rely on compliant, well-documented HRA processes and employee education on how to calculate HRA exemption and provide proof.

Common challenges and how to overcome them

Understanding how to calculate HRA exemption is straightforward, but real-world challenges appear frequently:

- Insufficient documentation: The absence of rent receipts or a bank trail causes claims to be reduced or rejected. Solution: maintain receipts, bank transfers, and a clear rent agreement.

- Payments to relatives: Paying rent to family members raises scrutiny; proof of genuine tenancy (independent bank transfers, separate lease, and evidence of independent living arrangements) helps guard against disallowance.

- Employer verification gap: Many employees assume HRA claimed in payroll is automatically safe; however, employers may refuse unverified claims. Solution: submit Form 12BB and required documents on time.

- Misunderstanding salary composition: Including non-eligible components in “salary” for calculation results in incorrect computations. Solution: confirm with payroll what constitutes salary for HRA calculation.

- Frequent relocations: Moving mid-year complicates annual computations. Solution: keep month-wise record, file accurate ITR, and retain proof for each location/month.

Authorities have increasingly required more detailed disclosures to curb misuse, so you must be prepared to substantiate claims. Recent media coverage highlights increased scrutiny and the need for accurate documentation. The Times of India+1

Employer perspective: payroll compliance and best practice

From the employer’s standpoint, knowing how to calculate HRA exemption is part of robust payroll governance:

- Implement standard HRA computation logic in payroll software: least of the three conditions (actual HRA, rent minus 10% of salary, and 50%/40% of salary).

- Collect and retain Form 12BB and rent proofs every year for audit readiness.

- Communicate clear guidance to employees about required documents and landlord PAN thresholds.

- Prorate HRA correctly for joiners, leavers, and in-year relocations.

Clear employer policies reduce errors and protect both parties during tax assessments.

Technology and tools: calculators and automation

Several tax portals and banks provide HRA calculators that automate the process of how to calculate HRA exemption. The Income Tax Department itself offers a calculator to estimate exempt/taxable HRA, while private platforms (tax advisory websites and insurers) run similar tools that also provide step-by-step guidance. Such tools are helpful, but always cross-check with payroll definitions and the Income Tax Department’s guidance. Income Tax India+1

Policy discussion and future prospects

HRA, as currently structured, balances tax relief for renters with safeguards against misuse. Policy debates center on whether HRA should be more tightly targeted (for lower-income workers), whether metro designations should be updated to reflect changing urban agglomerations, and how HRA interacts with affordable housing policy. Potential future prospects include:

- More digital trail requirements: Expect continued emphasis on bank-based proof and landlord PAN to ensure traceability.

- Refined definitions of metro: As cities expand, government may update the list of metros for HRA calculations.

- Integration with housing affordability initiatives: HRA policy could be calibrated to complement national or state affordable housing programs.

If you want to future-proof your financial planning, periodically review both central and state-level announcements relating to housing and tax policy.

Step-by-step checklist: before you file ITR

To ensure your HRA claim stands up to scrutiny and that you have correctly learned how to calculate HRA exemption, follow this checklist:

- Verify Basic + DA figure used by payroll for “salary”.

- Gather rent receipts and rent agreement for the financial year.

- Ensure bank trail for rent payments (NEFT/RTGS/cheque).

- Confirm the HRA component on payslips and Form 16 (if applicable).

- Submit Form 12BB and landlord details (PAN if needed) to employer.

- Recompute the HRA exemption using the least-of-three formula and report taxable portion in ITR.

- Retain copies of all proofs for at least the statutory assessment period.

Following this routine helps when you are asked to demonstrate how you calculated HRA exemption during employer verification or tax assessment. Income Tax India

FAQs — Common questions answered

Below are commonly asked questions about how to calculate HRA exemption with concise, authoritative answers.

Final checklist: practical tips to maximize legitimate HRA benefit

- Keep meticulous proof of rent payments and ensure they are consistent with rent receipts.

- Verify that payroll uses the correct salary base (Basic + DA as applicable).

- If you’re in a metro, remember the 50% rule — it often increases your exempt portion.

- When changing jobs, maintain continuity of documentation to avoid gaps.

- Consider overall tax planning: compare the HRA benefit vs home loan deductions when deciding to rent or buy.

Closing thoughts

Understanding how to calculate HRA exemption is a powerful tool in personal tax planning. It’s straightforward in principle — choose the least of three values — but in practice it demands careful attention to salary composition, clear documentation, and an awareness of regional and policy factors. Whether you are an HR professional handling payroll or a taxpayer filing your return, applying the formula correctly and keeping supporting proofs can prevent disputes and deliver meaningful tax savings.

For precise figures and the latest procedural updates, use the Income Tax Department’s official HRA calculator and consult your payroll team or a tax advisor to ensure your personal circumstances are correctly handled. Income Tax India+1