How to Calculate HRA Deduction: A Complete Guide for Salaried Taxpayers

House Rent Allowance (HRA) is one of the most commonly used tax benefits by salaried individuals in India. Understanding how to calculate HRA deduction correctly can lead to meaningful tax savings every financial year. This long-form guide explains the history, objectives, legal framework, calculation methods, state-level implications, success stories, challenges, comparisons with other tax reliefs, practical worked examples, and future prospects — all written to help you claim HRA accurately and confidently.

Introduction — why HRA matters

For millions of urban and semi-urban salaried employees, housing is a major monthly expense. To mitigate this burden, employers often include a House Rent Allowance component in salary structures. Knowing how to calculate HRA deduction is not merely an accounting exercise — it’s a way to keep more of your hard-earned income and plan personal finances better. The mechanics of HRA calculation balance salary components, rented accommodation costs, and tax rules, with additional considerations under the old and new tax regimes in India. Authoritative calculators and government tools exist to support taxpayers in this process. Income Tax India+1

A brief history and policy framework of HRA

HRA as a salary element and a tax exemption has evolved as part of India’s post-independence fiscal policy toolkit. The allowance was formalized to help salaried workers meet housing costs and to incentivize mobility for employment purposes. Over decades, HRA’s legal and computational framework has been refined through amendments to the Income Tax Act and through clarifications from the tax department. The principal statutory anchor for HRA exemption under the old regime has been Section 10(13A) of the Income Tax Act, which sets out the formula and conditions for exemption. For practical use, the government’s own HRA calculator implements the statutory “least of three” rule that governs the exempt portion. Income Tax India

Objectives of HRA exemption

HRA serves multiple objectives:

- Provide targeted relief for housing costs borne by salaried individuals.

- Encourage labor mobility by offsetting relocation costs.

- Reduce the effective tax burden for lower and middle-income employees.

- Support formal rental markets by incentivizing documented rent transactions.

While the allowance directly addresses urban housing affordability for employees, its ripple effects touch on regional housing demand, landlord income, and the broader fiscal ecosystem (for example, documentation and reporting standards). The interplay between HRA and broader social policy areas — such as women’s economic empowerment and rural-urban migration — can be indirect but significant when rent and employment patterns shift across states.

Legal eligibility: who can claim HRA?

A salaried employee whose salary explicitly includes an HRA component and who actually pays rent for residential accommodation is eligible to claim HRA exemption under the old tax regime. If you live in accommodation owned by you (or provided by the employer) or don’t actually pay rent, the HRA exemption does not apply. Importantly, taxpayers choosing the new tax regime (which offers lower rates but disallows most exemptions) cannot claim HRA exemption — in that regime, the HRA component is fully taxable. This is a critical decision point when planning whether to opt for the old or new tax regime. TaxBuddy.com+1

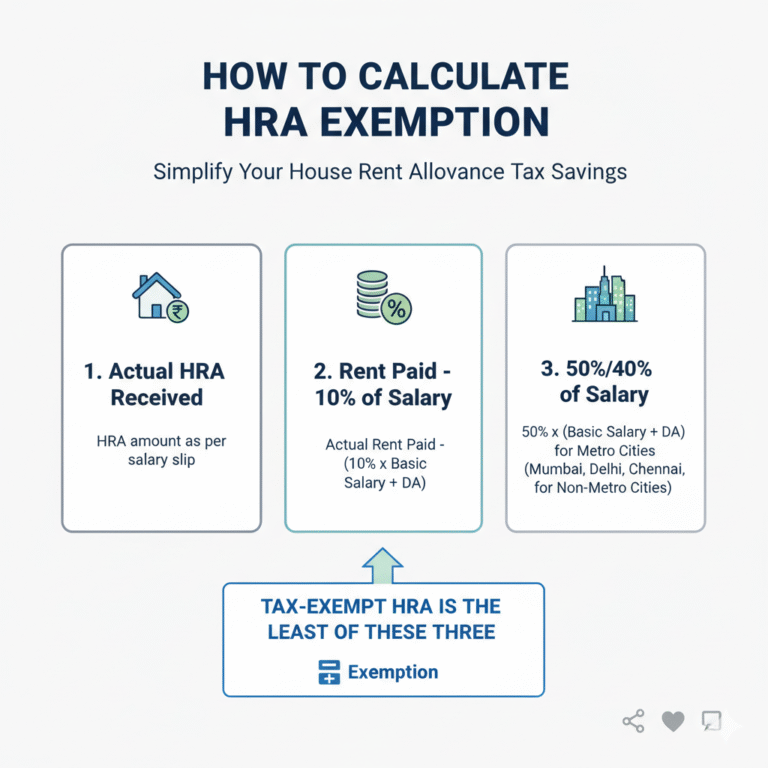

The formula — how to calculate HRA deduction (the statutory “least of three” rule)

At the heart of how to calculate HRA deduction is a simple but strict rule: the exempt portion of HRA is the least of the following three amounts:

- Actual HRA received from the employer during the financial year.

- Actual rent paid minus 10% of salary (salary here means basic salary plus dearness allowance that forms part of salary).

- 50% of salary if the residence is in a metro city (Delhi, Mumbai, Kolkata, Chennai) or 40% of salary if in a non-metro city.

Put differently, compute all three values and the exemption equals the smallest of them. Any HRA amount above the exempt portion is taxable and must be reported as taxable allowance. Government calculators and many tax portals implement this exact three-point test, so taxpayers can cross-check calculations using official and commercial tools. Income Tax India+1

Breaking down the components used in the formula

To apply the formula correctly you must understand what each term means:

- Actual HRA received: The aggregate HRA credited by the employer in your Form 16 or salary slips for the year.

- Actual rent paid: Total rent paid to landlord(s) during the year. If you pay rent to a relative or family member, additional documentary evidence of actual rent payment (bank transfer, receipts) strengthens the claim if questioned. Rent paid in cash is allowed but risky to substantiate during scrutiny.

- 10% of salary: The statutory test reduces rent by 10% of salary to account for personal contribution; salary for this purpose is basic pay plus dearness allowance (if any) that forms part of salary and commission if it is as a percentage of turnover.

- 50% or 40% of salary: Whether your city is treated as a metro affects the ceiling; metros have 50% ceiling while non-metros have 40%.

Understanding these terms helps you see why how to calculate HRA deduction is not simply about the rent but about salary composition and city classification.

Practical worked example (step-by-step)

Let’s walk through a stepwise worked example so you can practice the method for how to calculate HRA deduction.

Assumptions for the year:

- Basic salary + DA (forming part): ₹40,000 per month → ₹480,000 annual.

- HRA received: ₹15,000 per month → ₹180,000 annual.

- Rent paid: ₹12,000 per month → ₹144,000 annual.

- City: non-metro (40% rule).

Step 1: Actual HRA received = ₹180,000.

Step 2: Rent paid minus 10% of salary = ₹144,000 − 10% of ₹480,000 = ₹144,000 − ₹48,000 = ₹96,000.

Step 3: 40% of salary (non-metro) = 40% of ₹480,000 = ₹192,000.

Now pick the least of {₹180,000; ₹96,000; ₹192,000} = ₹96,000. So exempt HRA = ₹96,000. Taxable HRA = ₹180,000 − ₹96,000 = ₹84,000, which will be added to taxable income. This example clarifies precisely how to calculate HRA deduction in practice. For cross-checks, use the government’s HRA calculator or verified tax portals. Income Tax India+1

Metro vs non-metro: why city classification matters

As the formula shows, whether your workplace is in a metro city changes the 50% vs 40% benchmark, potentially increasing your exempt amount. This differentiation exists because living costs and rents are generally higher in metros, so the statutory ceiling accounts for that variation. If you live and work in a metro, you can claim up to 50% of salary as one of the comparative values — often increasing the exempt HRA value — but remember the final exemption still depends on the least-of-three rule. Official resources and employer HR policies typically identify whether your city is treated as a metro for HRA purposes. Income Tax India

Documentation and proof: what you should retain

While the Income Tax Return (ITR) does not require HRA proof to be uploaded in most cases, employers usually ask for rent receipts or a signed rent agreement during the year to compute HRA exemption in Form 16. Recent changes in ITR forms and compliance expectations have increased the requirement for detailed reporting; taxpayers should keep:

- Rent receipts signed by the landlord with PAN if annual rent exceeds specified thresholds.

- Bank transfer proof (cheques, NEFT/RTGS/UPI) showing payment of rent.

- Rent agreement specifying tenure and address.

- Landlord PAN details (if rent paid exceeds ₹1,00,000 per year, furnishing landlord PAN is often required by employer and the department).

Maintaining these documents reduces the risk of disallowance on scrutiny. Recent reporting requirements emphasize transparency in deduction claims. The Times of India+1

When HRA cannot be claimed — common exclusions

You cannot claim HRA exemption under the following situations:

- You live in accommodation owned by you and do not pay rent.

- Employer provides you with rent-free accommodation.

- You opt for the new tax regime for a given year (in which HRA exemption is unavailable).

- You do not have documentary proof (if requested by employer or during assessment scrutiny) to substantiate rent payments.

If you fall outside the HRA rules, a different route — Section 80GG — allows some relief for those who don’t receive HRA from employers, but that deduction has its own limits and conditions. TaxBuddy.com

Section 80GG — alternative for those without HRA

Employees who do not receive HRA from their employers (for example, self-employed individuals or salaried employees without HRA component) may be eligible to claim deduction under Section 80GG. The deduction under Section 80GG is the least of:

- ₹5,000 per month (₹60,000 annually),

- 25% of adjusted total income, or

- Actual rent paid minus 10% of total income.

To claim Section 80GG, the taxpayer must file form 10BA (self-declaration) and meet other conditions (not owning a house at the place of employment, etc.). Section 80GG provides an important alternative but is generally less beneficial than HRA computed under Section 10(13A) if you receive HRA from the employer. TaxBuddy.com

State-level impact and regional considerations

While HRA is a federal tax provision, state-level dynamics affect its real-world impact:

- State rental markets: High-rent states and metros drive larger HRA components in salary structures and greater exempt amounts for employees.

- Inter-state labor mobility: States with job clusters attract workers who rely on HRA to subsidize relocation costs.

- Documentation norms: In some states, landlord registration and municipal rental rules influence the ease of producing rent proof.

- State employee allowances: State governments often have their own HRA schedules for public servants which depend on city categories; these interact with central tax rules for exemption calculations. For example, certain state-level HRA notifications set specific percentages for HRA allowances paid to state employees based on the city/town category. punjabcivilrules.com

State-wise differences also intersect with social policy measures: if rental outcomes influence migration, they also interact indirectly with initiatives on women’s economic participation, rural development, and social welfare. For instance, affordable rental stock can encourage women to take jobs in cities, which aligns with broader empowerment objectives.

Success stories and scenario analyses

Several organizations and households have used accurate HRA computation to meaningfully improve disposable income:

- A young professional relocating from a small town to a metro negotiated a salary structure with a higher HRA component, using the HRA exemption calculation to offset urban rent.

- An employer standardized rent receipt submission through digitized HR portals, reducing disallowances and speeding up payroll computations.

- A family optimized finances by comparing the benefits of claiming HRA vs moving to a smaller owned property, quantifying savings after tax to decide.

These success stories show how understanding how to calculate HRA deduction translates into tactical decisions: negotiating CTC, choosing residence, and documenting rent properly.

Common challenges and points of friction

Despite the straightforward formula, practical challenges arise:

- Documentation mismatch: Rent agreements that don’t match payment records or landlord PAN absence can lead to denials.

- Payment methods: Cash rent is still common in many places but is harder to substantiate. Digital payment trails are preferable.

- Family arrangements: Paying rent to relatives can invite closer scrutiny. Evidence of market-rate rent and bank transfers help.

- New tax regime decision: Choosing between the old and new tax regimes requires a calculation of whether HRA and other exemptions outweigh the new regime’s lower rates.

- Employer practices: Incorrect salary structuring (HRA not a separate component) can prevent rightful claims.

Understanding these friction points helps taxpayers proactively reduce the risk of complications when claiming HRA.

Comparisons with other housing-related tax benefits

HRA is only one tool in a broader set of housing-related tax rules:

- Home loan interest and principal repayment: Sections 24(b) and 80C allow deductions for home loan interest and principal repayment; these primarily help homeowners rather than tenants.

- Section 80GG: As noted earlier, a fallback for those without an HRA component.

- Standard deduction: Separate from housing benefits; not linked to rent.

Comparing these options means assessing whether renting and claiming HRA is more tax-efficient than owning with loan-based deductions, depending on personal financial circumstances, interest costs, and long-term plans.

Practical checklist for taxpayers: prepare, compute, file

To ensure your HRA claim is smooth and defensible, follow this checklist:

- Ensure HRA is a separate salary component in your offer letter and payslips.

- Maintain clear rent receipts and bank transfer records for the entire financial year.

- Keep a signed rent agreement and, if applicable, the landlord PAN (for high rent).

- Compute exemption using the least-of-three rule and reconcile with Form 16.

- If switching tax regimes, compute tax liability under both regimes to choose optimally.

- Retain documents for at least the statutory assessment period (typically several years).

These steps directly support accurate outcomes when learning how to calculate HRA deduction.

Employers’ role and good practice

Employers are crucial in enabling compliant HRA claims:

- Clearly declare HRA in salary break-up and Form 16.

- Request and verify rent proofs before the year-end to calculate exemptions.

- Provide guidance on documentation thresholds and landlord PAN requirements.

- Offer digital portals for submitting receipts to maintain audit trails.

Proactive employer practices reduce disputes and increase employee confidence when claiming HRA.

How audits and scrutiny happen — and how to respond

Tax authorities may scrutinize HRA claims in selected cases. Typical triggers include disproportionate HRA claims relative to salary, rent paid to related parties, or mismatched documentation. If selected for scrutiny:

- Produce rent receipts, bank statements, rent agreements, and landlord PAN (if required).

- Demonstrate consistent payment patterns (e.g., standing instructions, UPI/cheque records).

- If rent was paid in cash, corroborating evidence such as signed receipts and third-party witnesses may help (though proof by bank transfer is better).

Good record-keeping and timely employer-provided documentation mitigate the risk of adverse outcomes. Recent tax utilities emphasize disclosure, so prepare files preemptively. The Times of India+1

Digital tools and calculators: cross-checking your numbers

Government and reputable private portals provide HRA calculators that implement the statutory computation and reduce human error. Use these tools to validate your manual calculation of how to calculate HRA deduction, and reconcile their output with your Form 16. The Income Tax Department’s official HRA calculator reflects the law and is a reliable source for verification. Income Tax India+1

Policy interactions: HRA and social objectives

Although HRA is a tax-specific allowance, it intersects indirectly with social and regional policy:

- Regional impact: HRA cushions relocation costs, enabling workforce mobility to growth centers and influencing urban housing demand patterns.

- Women’s economic empowerment: Affordable renting options supported by HRA can encourage women to accept jobs away from their natal homes.

- Rural development: If urban jobs beckon but housing barriers are high, HRA can play a role in migration patterns that affect rural economies.

- Social welfare initiatives: HRA operates alongside subsidies and housing schemes; coordinated policy can amplify benefits.

While not a direct welfare program, HRA’s fiscal design should be viewed within a broader policy framework that includes housing supply, rental law, and social inclusion.

International comparisons: HRA-like measures

Many countries provide tax reliefs or benefits connected to housing (e.g., mortgage interest deductions, rental subsidies, or relocation allowances). HRA’s distinct feature is its targeted exemption tied to an explicit salary component. Comparing structures internationally helps tax designers think about fairness, mobility incentives, and housing market effects.

The future of HRA — prospects and likely trends

Several trends could shape the future of HRA:

- Digitization and documentation: Increasing digital payments and stricter reporting rules make HRA claims more traceable and less disputed.

- Regime choices: The popularity of the new tax regime (which disallows HRA) may influence salary structuring and employee decisions. Taxpayers increasingly run comparative calculators to choose the optimal regime each year. TaxBuddy.com

- Policy convergence: As urban housing policy evolves, HRA may be rebalanced to align with affordable rental initiatives, or the logic of exemptions may be revisited for equity.

- State coordination: States might sync their housing allowances for public servants with central tax rules, increasing predictability for employees deployed across states.

Understanding these trajectories helps taxpayers and employers plan salary structures and housing choices with foresight.

Step-by-step guide: compute your HRA exemption today

- Gather: annual basic salary (plus DA if part of salary), total HRA received, total rent paid, and your city classification.

- Compute three values: (a) actual HRA received, (b) rent paid minus 10% of salary, (c) 50% or 40% of salary depending on metro status.

- The exempt HRA = least of the three values. Taxable portion = HRA received − exempt HRA.

- File your ITR reflecting taxable HRA in salary income and keep supporting documents.

- If you do not receive HRA, check Section 80GG rules and compute the eligible deduction using its own least-of-three test. Income Tax India+1

Frequently Asked Questions (FAQs)

Closing — make HRA work for you

Knowing how to calculate HRA deduction accurately is a high-ROI financial skill for salaried taxpayers. It requires careful attention to salary composition, rent documentation, and whether the old or new tax regime serves you better. Use government calculators, maintain clean records, and if needed consult a tax professional for complex situations (for example, rent paid to relatives or split-year employment). With the right approach, HRA can be a dependable tool to reduce tax liability and improve household cash flow — an objective directly linked to broader aims of mobility, economic participation, and fiscal efficiency.

For authoritative calculations, use the Income Tax Department’s official HRA calculator and reputable tax portals as a secondary cross-check. Income Tax India+1