HRA Calculator for ITR

Calculate HRA exemption for Financial Years 2021-22 to 2023-24

HRA Exemption for FY 2023-24

Calculation Breakdown

House Rent Allowance (HRA) is one of the most important components in the pay structure of salaried employees in India. For taxpayers, understanding hra calculation for itr is essential to claim accurate exemptions, reduce tax liability legally, and ensure a smooth income tax return (ITR) filing. This comprehensive guide explains the history, objectives, methodology, documentation, state-level nuances, implementation challenges, comparative frameworks, success stories, and future prospects surrounding hra calculation for itr. It is designed for tax professionals, HR personnel, salaried employees, and anyone seeking clarity on claiming HRA exemption while filing their ITR.

Understanding HRA: Background and Purpose

HRA, or House Rent Allowance, was introduced in India as a component of salary to provide relief to employees who rent accommodation. The allowance has a social and fiscal rationale: to support workforce mobility, encourage urban employment, and provide targeted tax relief to those incurring rental expenses. Historically, hra calculation for itr evolved through tax law clarifications and judicial interpretations, shaping how exemptions are determined and applied.

The basic purpose behind HRA and the related hra calculation for itr procedure is twofold: first, to compensate employees for housing costs, and second, to provide a tax-efficient mechanism that recognizes rental expenditures. Because India’s housing markets vary widely—metro cities versus smaller towns—the tax code allows a structured exemption formula that aims to be fair while remaining administratively manageable for tax authorities.

Legal Framework and Historical Evolution

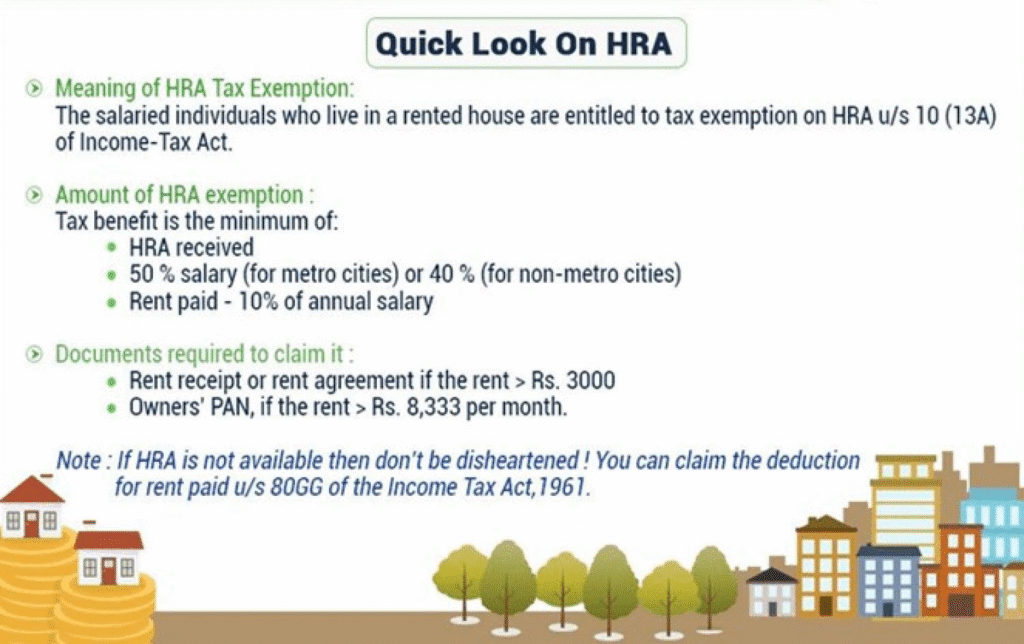

The HRA exemption is governed primarily by Section 10(13A) of the Income-tax Act, and the rules under the Income Tax Rulebook. Over time, administrative guidance and court judgments have clarified elements such as the treatment of dearness allowance, HRA for self-occupied versus rented properties, and documentation requirements for hra calculation for itr.

Initially, HRA was broadly permitted as a tax-free allowance within reasonable limits. As urbanization accelerated and rental markets diversified, the government tightened the framework to ensure the exemption targeted genuine rental expenses. Thus, the hra calculation for itr procedure crystallized into a standard formula, balancing simplicity with fairness.

Objectives of HRA and the HRA Calculation for ITR

The goals behind the HRA exemption and the hra calculation for itr process include:

- Reducing the tax burden for salaried individuals who actually incur housing costs.

- Promoting labor mobility by providing tax relief for employees who must relocate for work.

- Introducing a dependable, verifiable method for determining exemption amounts in income tax returns.

- Ensuring consistency across regions while allowing for differential treatment for metro cities and non-metros.

For taxpayers, understanding these objectives helps in appreciating why hra calculation for itr follows specific rules and why precise documentation is necessary.

The Formula: How HRA Calculation for ITR Works

The calculation for HRA exemption while filing ITR is formulaic and requires a few data points. The exempt portion is the minimum of these three values:

- Actual HRA received from the employer.

- Rent paid minus 10% of salary (where salary for this purpose includes basic salary plus dearness allowance if it forms part of retirement benefits).

- 40% of salary for non-metro cities or 50% of salary for metro cities (metro cities usually include Mumbai, Delhi, Kolkata, and Chennai; some interpretations may treat other cities as metros depending on the legislation).

A practical illustration of hra calculation for itr: suppose an employee receives an annual HRA of ₹120,000, pays annual rent of ₹180,000, and has an annual salary (basic + DA component included for this purpose) of ₹600,000. The three values for the formula would be:

- Actual HRA received = ₹120,000.

- Rent paid minus 10% of salary = ₹180,000 − 10% of ₹600,000 = ₹180,000 − ₹60,000 = ₹120,000.

- 50% of salary if metro = ₹300,000; if non-metro 40% = ₹240,000.

The least of these three values would determine the exempt portion. Thus, for this example, the exemption would be ₹120,000. This is the core of hra calculation for itr: a minimum-of-three approach that is straightforward but invites careful documentation.

Components and Definitions Used in the HRA Calculation for ITR

Clarity about component definitions is crucial for reliable hra calculation for itr:

- Basic Salary: The fixed base pay before allowances and benefits. It is central to the formula because both the “10% of salary” calculation and the 40%/50% threshold use salary as the base.

- Dearness Allowance (DA): When DA is part of retirement benefits, it is included in salary for the HRA computation; otherwise, it may be excluded depending on employer’s pay structure and tax guidance.

- HRA Received: The actual House Rent Allowance disbursed by the employer during the financial year.

- Rent Paid: The actual rent paid to a landlord, usually supported by rent receipts or bank transfer evidence; if the landlord’s PAN is furnished and rent exceeds prescribed limits, further compliance may be required.

- Metro vs Non-Metro: The higher 50% threshold applies to metro cities; taxpayers must correctly identify the place of residence for hra calculation for itr.

Accurate classification and calculation of these components ensure the exemption claimed on ITR is compliant and defensible.

Documentation and Evidence Requirements

Proper documentation is the backbone of a trustworthy hra calculation for itr claim. Tax authorities may scrutinize exemptions, and taxpayers must be ready to provide substantiation. Typical documents include:

- Rent receipts specifying landlord name, address, amount, and signature.

- Copy of rental agreement where applicable.

- Bank statements showing rent payments (especially preferable when rent is high).

- Landlord’s PAN if annual rent paid exceeds ₹1,00,000 (or the threshold specified by law).

- Employer-issued salary slips showing HRA component and basic salary.

- Form 12BA or employer declarations, and Form 16 supporting salary details for ITR.

Employers often require submission of rent receipts during the fiscal year to adjust TDS on salary; similarly, while filing ITR, taxpayers should retain these documents for future verification.

Step-by-Step HRA Calculation for ITR: Practical Workflow

To carry out hra calculation for itr methodically when preparing your income tax return, follow this workflow:

Start by collecting salary slips and annual Form 16 to establish basic salary and HRA received. Sum up the actual rent paid during the financial year. Decide whether your place of residence is a metro city for the 50% threshold. Calculate 10% of salary and subtract it from the total rent paid. Compute 40%/50% of salary based on location. Compare the three values—actual HRA, rent minus 10% of salary, and 40%/50% of salary—and pick the smallest. That result is the exempted amount to be entered while filing the ITR. Report the balance HRA as taxable income.

Maintaining the documents above and following this workflow will make your hra calculation for itr robust and audit-ready.

Special Cases and Nuances in HRA Calculation for ITR

There are situations where the standard hra calculation for itr requires nuanced handling:

- Partial Year Employment or Multiple Employers: If you change jobs during the year and receive HRA from multiple employers, calculate exemption for each employer separately using respective salary and HRA components, then aggregate appropriately.

- Joint Rentals or Shared Accommodation: If rent is split among roommates, claim HRA proportionate to the share of rent you personally pay. Documentation should reflect your specific payments.

- Living with Parents but Paying Rent: If you pay rent to a family member, ensure the rent agreement is genuine and the landlord’s PAN is provided if applicable. Transfer of rent via bank channels strengthens your claim.

- Self-Occupied Property and HRA: If you own a house and live in it, you cannot claim HRA. If you own property in one city but rent in another for work, the hra calculation for itr may still allow exemption if you genuinely pay rent.

- Concessional HRA and Reimbursements: Some employers reimburse rent under special schemes; ensure reimbursements are treated correctly in payroll to reflect in hra calculation for itr.

Understanding these special cases prevents errors and unexpected tax adjustments.

State-Level Impact and Regional Considerations

The effectiveness and perceived fairness of hra calculation for itr intersect with regional housing markets and state policies. Metro cities with high rents—Mumbai, Delhi, Bengaluru—make the HRA exemption particularly valuable, while in smaller towns the benefit may be modest.

State governments and municipal policies influence rental markets: rental control acts, urban development initiatives, and affordable housing schemes affect rent levels and, by extension, HRA claims. For example, states that invest in rental housing or create affordable housing corridors will indirectly influence how taxpayers approach hra calculation for itr. Additionally, professional mobility supported by state-level industrial development can lead to increased demand for rental housing, increasing the relevance of HRA in states experiencing job-driven migration.

An informed hra calculation for itr recognizes these dynamics: salary structures and HRA norms in Kolkata may differ from Hyderabad due to local living costs, and taxpayers should ensure their HRA computation reflects true economic realities.

Implementation: Employer Role and Payroll Practices

Employers play a pivotal role in facilitating correct hra calculation for itr. Payroll teams must accurately structure salary components, record HRA disbursements, and educate employees on documentation required for HRA exemption claims. Standard employer practices involve:

- Collecting rent proofs during the financial year.

- Adjusting TDS based on declared HRA exemptions.

- Issuing accurate Form 16 and salary slips showing HRA and basic pay components.

- Advising employees on submission of landlord PAN when thresholds trigger.

Automation in payroll systems can simplify hra calculation for itr by flagging inconsistencies, calculating exemptions in real-time, and generating reports for audit. Transparent employer practices reduce taxpayer errors and simplify subsequent ITR filing.

Challenges and Common Pitfalls in HRA Calculation for ITR

While the formula is straightforward, many taxpayers face common pitfalls during hra calculation for itr:

Incorrect salary definition: omitting or misclassifying dearness allowance where it should be included can skew calculations.

Incomplete documentation: lack of proper rent receipts, unsigned receipts, or cash payments can lead to disallowance during assessment.

Misidentifying metro status: applying 50% ceiling where the address does not qualify as metro results in underpayment of tax and potential penalties.

Paying rent to close relatives without legitimate documentation or bank transfers may raise questions about genuineness.

Failing to aggregate HRA properly in case of job change mid-year leads to incorrect exemption calculations.

Each of these pitfalls can be avoided by meticulous record-keeping and understanding the legal definitions involved in hra calculation for itr.

Comparisons: HRA vs Other Housing-Related Tax Benefits

HRA is one among several housing-related tax provisions. Comparing hra calculation for itr with other benefits clarifies choices taxpayers face:

- HRA vs Home Loan Interest Deduction: Home loan interest provides deduction under Section 24(b) and principal repayment under Section 80C. If you own a house and have a home loan, HRA cannot be claimed for that same house. Tax planning must determine whether renting and claiming HRA or living in the self-owned house with loan deductions results in greater tax efficiency.

- HRA vs Standard Deduction: Standard deduction for salaried employees is a fixed amount and unrelated to rent. Together, both can reduce taxable income but are applied differently.

- HRA vs Rent Receipts Deduction for Non-Salaried: Self-employed individuals cannot claim HRA but may be able to claim house-related expenses under business rules; their tax treatment differs.

Understanding these comparisons helps taxpayers decide personalized tax strategies, integrating hra calculation for itr with other housing tax benefits.

Success Stories: How HRA Calculation for ITR Helped Taxpayers

Across diverse Indian cities, many taxpayers have leveraged correct hra calculation for itr to achieve significant tax savings and streamlined audits. Consider a mid-level executive who relocated to a metro city and, by systematically submitting rent receipts and maintaining bank transfers, successfully claimed HRA exemption amounting to tens of thousands each year—lowering her taxable income and freeing cash flow for savings. In another example, an HR department introduced an automated rent verification system, which reduced employee errors and TDS mismatches, demonstrating how organizational practices support accurate hra calculation for itr.

These success stories point to a common theme: accurate documentation, timely submission of proofs, and clear payroll policies lead to optimal HRA exemption results and fewer disputes with tax authorities.

Policy Framework and Social Impact

Beyond individual tax savings, hra calculation for itr interacts with broader social objectives. By reducing tax burdens for renters, the policy indirectly supports labor mobility and urban workforce participation. It can also influence demand for rental housing, encouraging private investment in rental properties. When coordinated with state-level affordable housing schemes, HRA exemptions can be part of a holistic strategy addressing urban housing shortages.

Moreover, HRA-related policy debates often intersect with social welfare initiatives. Discussions about whether HRA disproportionately benefits higher-income salaried employees in expensive metros versus lower-income renters in smaller towns influence policy revisions and targeted housing programs.

Technological Tools and HRA Calculation for ITR

Technology is improving the reliability and convenience of hra calculation for itr. Payroll software can calculate exemptions automatically, generate rent proof checklists, and integrate with employee self-service portals to collect receipts. Tax filing platforms prompt users for HRA details and validate the entries against employer-provided Form 16 data, reducing input errors.

For HR departments, cloud-based solutions can maintain landlord PAN details, tie rent payments to bank transfers, and produce audit-ready reports—making hra calculation for itr much easier to support and defend.

International Perspectives: How Other Countries Treat HRA-Like Benefits

While India has a distinct HRA mechanism, comparing it to international models illuminates alternative approaches. Some countries offer housing allowances with specific tax treatments, while others provide deductions or credits based on mortgage interest. The Indian hra calculation for itr blends allowance-based relief with objective formulas, a hybrid that balances administrative simplicity and targeting. Learning from global practices may inspire refinements to make the system more equitable or easier to implement across different urban contexts.

Enforcement, Audits, and Compliance

Tax authorities periodically scrutinize HRA claims during assessments. Accurate hra calculation for itr, supported by robust documentation, reduces exposure to reassessments. Common audit triggers include large HRA claims relative to income, cash rent payments without bank evidence, or conflicting employer records.

To stay compliant, taxpayers should ensure consistency between employer-submitted data and ITR entries, keep rent receipts for at least the statutory period, and be prepared to furnish landlord PAN when required. Employers should reconcile payroll data and ensure accurate Form 16 issuance to avoid mismatches.

Future Prospects: How HRA Calculation for ITR Might Evolve

The future of hra calculation for itr may be shaped by policy reforms, digitization of rent records, and urban housing strategies. Possible directions include:

- Enhanced digital rent registers linking tenant and landlord financial records to simplify proof.

- Revised thresholds or expanded metro definitions reflecting changing urban dynamics.

- Integration of HRA processing within unified tax-filing platforms, reducing manual data entry and errors.

- Policy adjustments to better balance benefits across income groups and geographies, possibly introducing targeted subsidies for low-income renters.

Regardless of the direction, digitization and policy alignment with housing initiatives are likely to make hra calculation for itr more transparent and efficient.

Practical Tips for Taxpayers: Optimizing HRA Calculation for ITR

To make the most of hra calculation for itr, taxpayers should:

- Keep organized rent receipts and bank transfer evidence.

- Ensure HRA receipts and employer records match ITR entries.

- Understand whether DA should be included in salary for exemptions.

- Collect landlord PAN when rent thresholds require it.

- When changing jobs, calculate HRA exemption for each employer period.

- Use employer-hosted payroll portals to submit rent proofs timely.

These practical steps will safeguard your exemption claims and simplify future tax interactions.

Integrating HRA Calculation for ITR with Broader Tax Planning

HRA should be considered as part of comprehensive tax planning. Evaluate HRA claims alongside investments under Section 80C, home loan deductions, and other salary exemptions. For families with dual-income earners or complex living arrangements, coordinated planning can yield optimized tax outcomes. Financial advisors and tax professionals often model scenarios—renting with HRA exemption versus buying a home with mortgage benefits—to determine the most tax-efficient choice for an individual’s life stage and long-term goals.

Case Study: A Comparative Scenario

Consider two professionals: one working in a Tier-1 metro paying high rent and another in a smaller city with modest rent. Both earn similar basic salaries. Through accurate hra calculation for itr, the metro-based professional claims a larger exemption due to higher rent and the 50% salary threshold, significantly reducing taxable income compared to the non-metro peer. However, when mortgage deductions, long-term appreciation, and lifestyle preferences are included, the optimal financial decision may differ. This case underscores why precise hra calculation for itr is necessary but not the only factor in housing and tax choices.

Moving Beyond the Formula: Ethics and Best Practices

Proper hra calculation for itr is more than number-crunching. Ethical compliance—avoiding fabricated receipts, ensuring genuine landlord-tenant arrangements, and maintaining accurate employer disclosures—preserves the integrity of the tax system. Best practices include transparent record-keeping, timely submission of proofs, and consultation with tax professionals when in doubt.

Frequently Asked Questions

Conclusion: Mastering HRA Calculation for ITR

Understanding hra calculation for itr empowers taxpayers to claim rightful exemptions, plan housing decisions with tax efficiency in mind, and avoid common compliance pitfalls. From the underlying legal framework to practical payroll practices, the process requires attention to documentation, accurate salary component classification, and regional considerations. Employers and employees alike benefit from clarity and digitization in handling HRA matters. With transparent records, proactive tax planning, and adherence to guidelines, HRA remains a valuable tool in the salaried taxpayer’s financial toolbox.