HRA Tax Exemption Calculator

Calculate your House Rent Allowance tax exemption easily

1. Actual HRA received

2. 50% of salary (metro) or 40% (non-metro)

3. Excess of rent paid over 10% of salary

House Rent Allowance (HRA) remains one of the most valuable salary components for millions of salaried taxpayers. Understanding hra tax calculation is essential not only for effective tax planning but also for meaningful cash-flow management. This long-form guide explains the history, objectives, and legal framework behind HRA, provides a step-by-step hra tax calculation method, examines state-level and regional impacts, highlights implementation challenges and success stories, compares HRA to alternative housing reliefs, and looks at future prospects. Read on for an authoritative, practical, and SEO-optimized walkthrough designed to help you claim HRA correctly and confidently.

What is HRA and why it matters

House Rent Allowance (HRA) is a portion of salary paid by employers to employees to meet the cost of rented accommodation. While HRA is taxable in principle, the Indian tax law allows a portion of it to be exempt from income tax under Section 10(13A) read with Rule 2A of the Income Tax Rules when specific conditions are satisfied. A clear grasp of hra tax calculation helps taxpayers determine how much of their HRA is truly tax-exempt and how much will be added to taxable income.

The exemption reduces taxable salary, which lowers the income tax liability for the employee. For employees living in rented accommodation, an optimized hra tax calculation can translate into a meaningful annual savings — especially in high-rent metros.

(Authoritative sources confirm that the HRA exemption is determined under Section 10(13A) and Rule 2A of the Income Tax Act/Rules. )Income Tax India+1

Historical context and policy objectives

HRA emerged as a component of modern salaried compensation during the expansion of organized employment in the mid-20th century. It was intended to:

- Help employees meet rental housing costs without eroding disposable income.

- Serve as a fair component of in-kind compensation given urban rental pressures.

- Encourage private sector employers to assist employee housing affordability indirectly.

Over time, hra tax calculation rules evolved into a formal exemption mechanism to balance fairness across taxpayers and to avoid double benefits where employees already own homes or receive other housing subsidies. The policy objective has always been to provide targeted relief to salaried renters, while preventing misuse through clear documentation and limits.

Legal framework: Section 10(13A) and Rule 2A (high-level)

The legal basis for HRA exemption in India is Section 10(13A) of the Income Tax Act, read with Rule 2A of the Income Tax Rules. The exemption is available only under the old tax regime; the new tax regime (introduced with optional lower slab rates) typically does not allow HRA exemption, which means HRA becomes fully taxable if you opt for the new regime. This distinction is crucial when you do your hra tax calculation and decide which tax route to take for the assessment year.Income Tax Department+1

Rule 2A sets out the method for calculating the exempt portion of HRA. Practically, the exemption is the least of these three amounts:

- Actual HRA received from the employer.

- Rent paid in excess of 10% of “salary.”

- 50% of salary (for residents of metro cities — Delhi, Mumbai, Kolkata, Chennai) or 40% of salary (for residents of non-metro cities).

The Income Tax Department and many tax guides reiterate this three-point rule as the backbone of hra tax calculation.TaxTMI+1

Defining “salary” and rent for HRA purposes

A careful hra tax calculation depends on how “salary” and “rent paid” are defined in tax law:

- “Salary” for the purposes of HRA exemption generally means basic salary plus dearness allowance (DA) — but only if DA forms part of retirement benefits — and includes commission based on a fixed percentage of turnover where applicable. Other allowances and perks are typically excluded when computing the salary figure for HRA exemption.TaxBuddy.com+1

- “Rent paid” must be genuine: it is the rent you actually pay to the landlord. Where rent is paid to a relative, or where cash transactions lack supporting bank evidence, the tax department may scrutinize the claim. Recent enforcement and reporting trends underline the importance of authentic documentation for any hra tax calculation that relies on rent receipts.The Economic Times

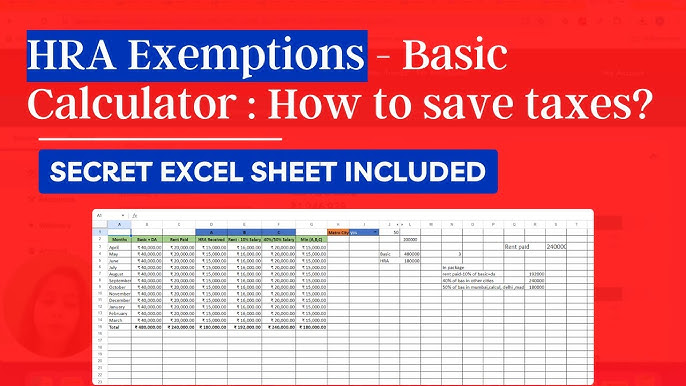

Step-by-step HRA tax calculation (practical walkthrough)

Below is a clear, practical method you can follow to perform your own hra tax calculation for a financial year. Use your annualized numbers (monthly amounts ×12) for consistency.

- Determine Annual Figures:

- Annual Basic Salary (and qualifying DA): Basic × 12.

- Annual HRA Received: HRA per month × 12.

- Annual Rent Paid: Rent per month × 12.

- Compute three candidate exemption amounts:

- A = Actual HRA received in the year.

- B = (Annual Rent Paid) − 10% of (Annual Salary).

(If this value is negative, treat it as zero.) - C = 50% of Annual Salary (if metro) OR 40% of Annual Salary (if non-metro).

- Exempt HRA = Minimum(A, B, C).

- Taxable HRA = Annual HRA Received − Exempt HRA.

- Final taxable salary is adjusted by replacing the gross HRA with taxable HRA; compute tax on the revised taxable income.

Example (simple numbers for clarity):

- Basic = ₹30,000 per month → Annual = ₹360,000.

- HRA = ₹15,000 per month → Annual HRA = ₹180,000.

- Rent Paid = ₹18,000 per month → Annual Rent = ₹216,000.

- Suppose resident in metro → C = 50% of Annual Salary = ₹180,000.

- B = ₹216,000 − 10% of ₹360,000 (₹36,000) = ₹180,000.

- A = ₹180,000. So Exempt = Min(₹180,000, ₹180,000, ₹180,000) = ₹180,000. Taxable HRA = ₹0.

This stepwise method forms the operational backbone for any accurate hra tax calculation, and many online calculators adopt the identical approach.ClearTax+1

Metro vs non-metro distinctions and state/city implications

A central parameter in hra tax calculation is whether you live in a “metro” city. Tax rules typically treat Delhi, Mumbai, Kolkata, and Chennai as metros, attracting the higher 50% salary slab for exemption; other cities fall under the 40% slab. This differential recognizes the greater rental burden in selected urban centres.

However, practical state-level and city-level dynamics can complicate calculations:

- Rapid urbanization and rising rents in Tier-2 cities sometimes make the 40% slab relatively less generous for residents of those cities. Where rental inflation accelerates, employees may find that hra tax calculation yields little or no exemption even though living costs are comparable to smaller metros.

- Employers operating across multiple states may have different payroll policies; some companies structure CTC with higher HRA components in high-rent locations. Understanding local rent patterns helps employees negotiate salary structures that maximize the advantage when doing their hra tax calculation.

Articles and tools from financial institutions explain this metro/non-metro split and list the cities conventionally counted as metros for hra tax calculation purposes.Housing+1

Documentation: what you must keep for safe claims

Proofs you should keep when relying on HRA exemption for hra tax calculation:

- Rent receipts: Signed receipts from your landlord showing period and amount.

- Rent agreement: A valid rental contract covering the financial year.

- Bank proof: Bank transfers, cheques, or other traceable evidence of actual payment.

- PAN of landlord: If rent paid in a year exceeds ₹1 lakh, you are required to provide the landlord’s PAN to the employer (as a compliance requirement in India).

- Employer declarations: Many employers require a declaration from the employee and copies of receipts before permitting the HRA exemption in payroll.

Keep authentic and consistent proof. Recent reporting and tax department actions show that HRA claims may be challenged if documents are missing, inconsistent, or appear contrived. Maintaining robust proof is essential to support any hra tax calculation shown in your returns.The Economic Times+1

Common pitfalls and red flags to avoid

When calculating HRA, taxpayers frequently stumble on a few recurring issues. Avoid these when doing your hra tax calculation:

- Using gross salary instead of “salary” (basic + qualifying DA) for the 10% and 40/50% computations. Only qualifying components count.TaxBuddy.com

- Failing to annualize figures correctly (e.g., mixing monthly and annual numbers).

- Not verifying whether DA qualifies for HRA computations (only DA that forms part of retirement benefits counts).

- Submitting rent receipts that lack corroboration through bank transfers or that are paid to close relatives without adequate justification.

- Choosing the wrong tax regime without simulating the impact on HRA — under the new regime HRA exemption is not available.

Avoiding these mistakes ensures a clean and defensible hra tax calculation.

Strategic salary structuring: legitimate techniques to optimize HRA benefits

Employees and employers can lawfully structure compensation to make HRA more effective, provided the arrangement is genuine and transparent. Some commonly used, legitimate strategies include:

- Negotiating a higher HRA component in CTC when relocating to high-rent cities. Since actual HRA received caps the exemption, a higher HRA will not hurt and can increase exempt amounts if rent supports it.

- Ensuring basic salary is not artificially depressed in a way that reduces 10% threshold benefits — remember the 10% subtraction uses salary (basic + qualifying DA), so basic plays a role.

- Maintaining precise rent payment records to support a claim that rent paid exceeds 10% of salary, thereby improving the second criterion in hra tax calculation.

- For employees moving between rented accommodations within a financial year, carefully annualize rent and HRA for each occupation period and maintain separate receipts/agreements.

All structuring must respect arm’s length principles and avoid fabrication; the tax authorities actively examine suspicious arrangements. When in doubt, document everything and consider professional tax advice to ensure your hra tax calculation and salary structuring remain compliant.

HRA and the new tax regime: impact on your calculation and choice

A crucial decision many taxpayers face is whether to opt for the new (optional) tax regime with lower slab rates and fewer exemptions, or to stay with the old regime and continue claiming exemptions like HRA. Because the HRA exemption is not typically available in the new tax regime, your hra tax calculation under the old regime may produce substantial tax savings if:

- You have significant genuine rent expenses, and

- Your HRA exemption under Rule 2A reduces taxable income enough to offset benefits of the new regime’s lower rates.

Taxpayers should run a side-by-side simulation: compute tax liabilities under both regimes — including a precise hra tax calculation for the old regime — before making the election. The Income Tax Department and many tax advisory portals provide comparison tools to help with such decisions.Income Tax Department+1

State-level and regional considerations (including wider development keywords)

Although HRA is a federal income tax provision, its effects ripple into regional and state-level economic patterns. When you do an hra tax calculation, think beyond the immediate tax number and consider these broader impacts:

- Regional impact: Higher HRA exemptions in metro cities aim to recognize urban rent pressures; however, they also influence where employers locate talent and how employees choose to relocate.

- Policy framework: State housing policies (e.g., rent control, affordable housing schemes) and central government housing programs indirectly interact with HRA benefits by shaping rental markets.

- State-wise benefits: Some states offer living subsidies, housing grants, or public housing stock that reduce dependency on private rent; where such benefits are strong, the practical impact of hra tax calculation may be less acute.

- Social welfare initiatives and women empowerment schemes: Governments sometimes focus on housing for marginalized groups; while those initiatives are not HRA per se, greater public housing access can alter market rents and therefore the practical value of HRA exemptions.

- Rural development: HRA is primarily urban-centric, but broader rural development can slow urban migration, influence rental demand, and thereby affect typical hra tax calculation outcomes in tier-1 and tier-2 cities.

Including these LSI terms in your broader financial planning can help you understand how individual hra tax calculation outcomes connect to larger policy and regional trends.

Success stories: when smart HRA planning delivered results

Several anonymized, real-world patterns show how careful hra tax calculation and documentation produced meaningful benefits:

- A young professional relocating to Mumbai negotiated a higher HRA component in CTC, maintained bank-transfer proofs for rent, and optimized tax liability by choosing the old regime. The result was a materially lower tax bill that justified the higher HRA structure.

- A family with multiple relocations tracked rent receipts and split calculations by occupancy period; by aggregating exemptions accurately using the stepwise hra tax calculation, they avoided under-claiming and reduced tax leakage.

- Employers who proactively provide HRA certificates and maintain transparent payroll computations reduce disputes and accelerate claims processing for employees, increasing net after-tax salary satisfaction.

These success patterns emphasize disciplined record-keeping and intelligent salary conversations with employers as key elements of a winning hra tax calculation strategy.

Challenges and enforcement realities

While HRA is a legitimate and enduring benefit, several challenges persist:

- Documentation abuse: Instances of fabricated rent receipts and payments to relatives have led to scrutiny and reassessment. Tax authorities have penalized false claims in the past. Transparent bank-based rent payments reduce this risk.The Economic Times

- Inconsistencies in employer practices: Some employers may not disclose HRA as a separate component or may treat payroll differently across offices, complicating employee hra tax calculation and claims.

- Migration and short-term rentals: Short stays, sublets, and co-living arrangements complicate the definition of rent paid and the continuity of claims. Employees must document the actual period of occupancy for accurate hra tax calculation.

- Ambiguities around DA and commission inclusion: Determining what qualifies as “salary” for HRA can be technical; changes in pay structure require fresh computation and possible recalibration of hra tax calculation.

These realities reinforce the importance of caution and professionalism when preparing any HRA claim.

Comparisons: HRA vs other housing-related tax benefits

HRA is not the only tax instrument addressing housing costs. Compare and contrast when performing broader tax planning:

- HRA vs Standard Deduction/New Regime: The new tax regime simplifies taxes but removes exemptions like HRA. Your hra tax calculation under the old regime vs the simplicity of the new regime must be compared numerically.Income Tax Department

- HRA vs Section 80C/80EE/80EEA home loan benefits: If you own a house with a home loan, you can benefit from principal repayment deduction under Section 80C and interest deductions under other sections — different kinds of relief than HRA, which applies only to renters. Sometimes owning plus loan benefits combined beat the HRA exemption, but costs and liquidity differ.

- HRA vs 80GG: Self-employed individuals who do not receive HRA can claim deduction under Section 80GG subject to conditions; the mechanics differ from hra tax calculation under Section 10(13A).

Understanding tradeoffs ensures that your housing strategy is tax-efficient and aligned with your life plans.

Technology and tools: calculators and payroll integration

In practice, most taxpayers use online HRA calculators that implement the Rule 2A logic for hra tax calculation. Employers often integrate HRA computations into payroll systems, performing monthly pro rata calculations and withholding tax accordingly.

When you use a calculator or payroll output, verify these points:

- Confirm the calculator uses Basic + qualifying DA for “salary.”

- Ensure the metro/non-metro choice is correct.

- Cross-check annualized numbers if you moved mid-year.

Using reliable calculators or payroll integrations reduces errors and improves accuracy in your hra tax calculation. Financial institutions and tax portals maintain HRA calculators aligned with Rule 2A.ClearTax+1

Future prospects and likely trends

As urban housing markets evolve and tax policy debates continue, several trends may affect hra tax calculation going forward:

- Policy reform debates: Tax policymakers periodically reassess deduction regimes. Any change to HRA rules would require legislative or regulatory updates. Taxpayers should monitor official notifications and credible policy commentary.Income Tax Department

- Digital evidence and compliance: Greater use of digital payments and e-records makes it harder to fabricate rent receipts, potentially tightening enforcement but also making legitimate claims easier to substantiate.

- Rental housing markets: If public housing supply improves or rent control remains a focus, the effective economic value of HRA could shift regionally, affecting typical hra tax calculation outcomes in different states.

- Increased payroll standardization: Employers may adopt uniform HRA approaches across branches, simplifying employee understanding of hra tax calculation.

Staying aware of these trends will help employees and advisors anticipate changes that affect HRA planning.

Ethical and compliance considerations

While HRA is a beneficial provision, ethical use and full compliance are essential:

- Claim only legitimate rent and genuine HRA receipts.

- Provide accurate landlord PAN where required.

- Do not fabricate receipts or manipulate arrangements solely to optimize hra tax calculation. Noncompliance carries penalties and reputational risk.The Economic Times

A responsible approach protects you from disputes and ensures the long-term sustainability of the HRA benefit.

Practical checklist before filing your tax return

Before you file returns and claim HRA exemption based on your hra tax calculation, complete this checklist:

- Annualize basic salary, HRA received, and rent paid.

- Confirm whether your DA qualifies to be included in “salary.”Income Tax India

- Decide old vs new tax regime after side-by-side computation.Income Tax Department

- Keep rent receipts, rent agreement, and bank proofs.

- Obtain landlord PAN where applicable.

- Ensure employer’s Form 16 reflects the exempt portion correctly (if employer processed it).

- If audited, be ready to produce documentation that supports your hra tax calculation.

Final thoughts: getting HRA calculation right

Mastering hra tax calculation is both a technical and practical exercise: you need to know the rules and you must maintain disciplined documentation. For the salaried renter, HRA remains a tax-efficient relief when legitimately claimed and properly supported. Combine intelligent payroll structuring, timely record-keeping, and careful regime choice to make the most of the HRA provision.

If you are uncertain about any specific element—how to treat DA, how to account for multiple relocations, or how to model new vs old regime outcomes—consult your payroll administrator or a qualified tax advisor. A small investment in clarification can yield meaningful savings in tax and peace of mind.